Laws, Regulations and Annotations

Search

Business Taxes Law Guide—Revision 2024

Sales And Use Tax Regulations

Title 18. Public Revenues

Division 2. California Department of Tax and Fee Administration — Business Taxes (State Board of Equalization — Business Taxes — See Chapters 6 and 9.9)

Chapter 4. Sales and Use Tax

Article 7. Specific Kinds of Property and Exemptions Generally

Regulation 1598.1

Regulation 1598.1. Diesel Fuel Prepayment Exemption.

Reference: Sections 6357.1, 6480, 6480.1, 6480.3, and 60022, Revenue and Taxation Code.

(a) Definitions.

(1) "Bulk deliveries" mean transfers of diesel fuel into storage tanks holding 500 gallons or more.

(2) "Cardlock, keylock, or other unattended mechanism" means an unattended, completely automated fueling station at which a purchaser obtains diesel fuel through use of a coded card or key and an access code. Charges for sales of diesel fuel to customers are usually consolidated at a central location and periodically invoiced to the purchaser.

(3) A "diesel fuel consumer" or "diesel fuel consumers" mean a person or persons that use diesel fuel in a manner that qualifies for the partial sales and use tax exemption set forth in Revenue and Taxation Code section 6357.1 and Regulation 1533.2, Diesel Fuel Used in Farming Activities or Food Processing.

(4) "Diesel fuel," for purposes of the imposition of the prepayment of sales tax, is defined in Revenue and Taxation Code section 6480(c) (by reference to Revenue and Taxation Code section 60022) and means any liquid that is commonly or commercially known or sold as a fuel that is suitable for use in a diesel-powered highway vehicle. A liquid meets this requirement if, without further processing or blending, the liquid has practical and commercial fitness for use in the engine of a diesel-powered highway vehicle. However, a liquid does not possess this practical and commercial fitness solely by reason of its possible or rare use as a fuel in the engine of a diesel-powered highway vehicle.

Diesel fuel does not include gasoline, kerosene, liquefied petroleum gas, natural gas in liquid or gaseous form, or alcohol.

(5) "Qualified retailer" means a person who meets the requirements of subdivisions (b)(1) through (b)(5).

(6) "Seller" means either the supplier or the wholesaler, as those terms are defined in Revenue and Taxation Code section 6480(c), that sells diesel fuel to a qualified retailer.

(7) "Total taxable sales" means the gross receipts from the sale of tangible personal property subject to tax, including sales of diesel fuel.

(b) Application of Tax. Commencing on and after October 9, 2002, a seller of diesel fuel is not required to collect the prepayment of sales tax on that percentage of diesel fuel specified in the retailer's diesel fuel prepayment exemption certificate that is otherwise required by Revenue and Taxation Code section 6480.1, provided the diesel fuel is sold to a retailer who:

(1) Will resell the diesel fuel in the ordinary course of business,

(2) Issues a diesel fuel prepayment exemption certificate to the seller as set forth in subdivision (c),

(3) Sells diesel fuel to a diesel fuel consumer,

(4) During the calendar year immediately preceding any purchases of diesel fuel, sold diesel fuel to diesel fuel consumers in which the gross receipts from such sales exceeded 25 percent of that retailer's total taxable sales, and

(5) Sold more than 50% of its diesel fuel through bulk deliveries or through a cardlock, keylock, or other unattended mechanism, or both.

For purposes of calculating the percentage set forth in subdivision (b)(4) above, the numerator shall be the sum total of amounts subject to the partial state tax exemption for diesel fuel used in farming and food processing for each return filed during the preceding calendar year and the denominator shall be the sum total of amounts subject to county tax for each return filed during the preceding calendar year.

(c) Prepayment Exemption Certificate.

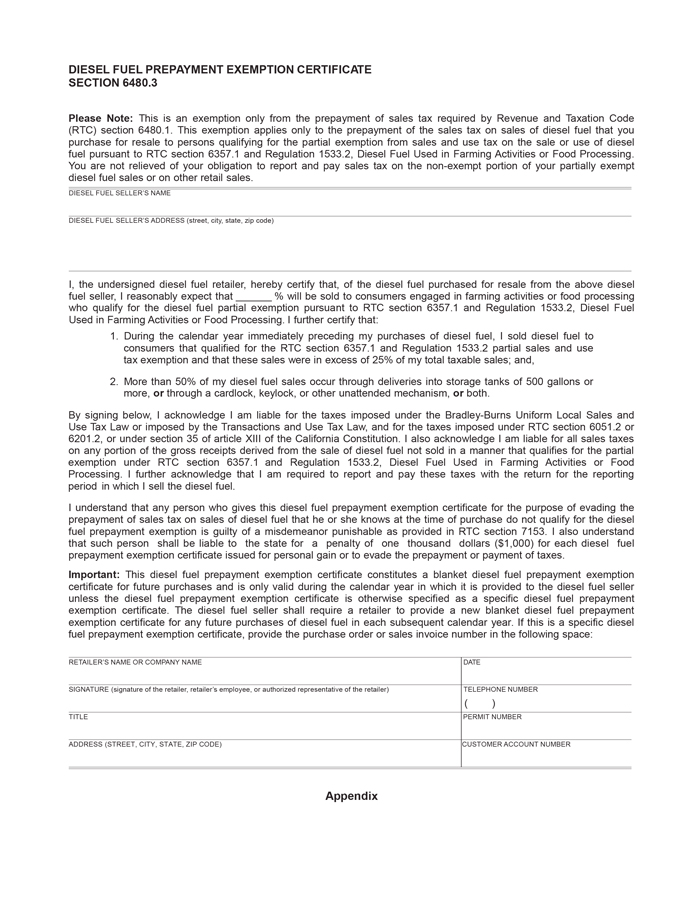

(1) In General. A seller of diesel fuel who takes a diesel fuel prepayment exemption certificate timely and in good faith, as defined in subdivision (c)(5), from a qualified retailer, is relieved from the liability for the sales tax prepayment subject to the exemption under this regulation, or the duty of collecting the sales tax prepayment subject to exemption under this regulation. A diesel fuel prepayment exemption certificate will be considered timely if it is taken any time before the seller bills the qualified retailer for the diesel fuel, any time within the seller's normal billing or payment cycle, or any time at or prior to delivery of the diesel fuel to the qualified retailer. A diesel fuel prepayment exemption certificate which is not taken timely will not relieve the seller of the liability for the sales tax prepayment excluded by the exemption; however, the seller may present satisfactory evidence to the Board that the seller sold the diesel fuel to a qualified retailer. A diesel fuel prepayment exemption under this part shall not be allowed unless the seller claims the exemption on its sales and use tax return for the reporting period during which the transaction subject to the diesel fuel prepayment exemption occurred. The diesel fuel prepayment exemption certificate form set forth in the Appendix may be used to claim the diesel fuel prepayment exemption.

(2) Blanket Prepayment Exemption Certificate. In lieu of requiring a diesel fuel prepayment exemption certificate for each transaction, a qualified retailer may issue a blanket diesel fuel prepayment exemption certificate. The diesel fuel prepayment exemption certificate form set forth in the Appendix may be used as a blanket diesel fuel prepayment exemption certificate. The diesel fuel prepayment exemption certificate in the Appendix may also be used as a specific diesel fuel prepayment exemption certificate if the qualified retailer provides the purchase order or sales invoice number and a precise description of the property being purchased. A blanket diesel fuel prepayment exemption certificate is only valid during the calendar year in which it is provided to the seller.

(3) Form of Prepayment Exemption Certificate. Any document, such as a letter or purchase order, timely provided by the qualified retailer to the seller will be regarded as a diesel fuel prepayment exemption certificate with respect to the sale of diesel fuel if it contains all of the following essential elements:

(A) The signature of the qualified retailer, qualified retailer's employee, or authorized representative of the qualified retailer.

(B) The name, address and telephone number of the qualified retailer.

(C) The number of the seller's permit held by the qualified retailer.

(D) A statement setting forth the requirements of subdivisions (b)(1) through (b)(5).

(E) A statement of what percentage of total diesel fuel purchases will be resold to diesel fuel consumers.

(F) Date of execution of document.

(4) Retention and Availability of Prepayment Exemption Certificates. A seller must retain each diesel fuel prepayment exemption certificate received from a qualified retailer who purchases diesel fuel for resale to diesel fuel consumers for a period of not less than four years from the date on which the qualified retailer claims an exemption for sales tax prepayment based on the diesel fuel prepayment exemption certificate. The Board may require, within 45 days of the Board's request, sellers to provide the Board access to any and all diesel fuel prepayment exemption certificates, or copies thereof, accepted for the purposes of supporting the diesel fuel prepayment exemption.

(5) Good Faith. A seller will be presumed to have taken a diesel fuel prepayment exemption certificate in good faith in the absence of evidence to the contrary. However, a diesel fuel prepayment exemption certificate cannot be accepted in good faith where the seller has knowledge that the diesel fuel will not be sold to a retailer who meets the requirements of subdivisions (b)(1) through (b)(5), will not otherwise be used by diesel fuel consumers, or that the percentage listed on the exemption certificate for sales tax prepayment is inaccurate. A blanket diesel fuel prepayment exemption certificate utilized for sales occurring in a subsequent calendar year in which the blanket diesel fuel prepayment exemption certificate was initially provided to the seller is not accepted in good faith for sales occurring in that subsequent calendar year.

(d) Retailer's Liability for the Payment of Tax.

(1) A qualified retailer providing a diesel fuel prepayment exemption certificate pursuant to subdivision (c) is liable for the taxes imposed by the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, and the tax that is imposed under Revenue and Taxation Code section 6051.2 or 6201.2, or under section 35 of article XIII of the California Constitution on the sale of diesel fuel to diesel fuel consumers.

(2) A qualified retailer providing a diesel fuel prepayment exemption certificate pursuant to subdivision (c) is liable for sales tax on any portion of the gross receipts derived from the sale of diesel fuel that is not sold to diesel fuel consumers.

(3) A qualified retailer that is liable for the tax under the provisions of subdivisions (d)(1) or (d)(2) shall report and pay that tax with the sales and use tax return filed for the reporting period during which the qualified retailer sells the diesel fuel.

(e) Improper Use of Prepayment Exemption Certificate. Any person who gives a diesel fuel prepayment exemption certificate pursuant to this regulation for the purpose of evading the prepayment of sales tax on sales of diesel fuel that he or she knows at the time of sale do not qualify for the diesel fuel prepayment exemption is guilty of a misdemeanor punishable as provided in Revenue and Taxation Code section 7153. In addition, such person shall be liable to the state for a penalty of one thousand dollars ($1,000) for each diesel fuel prepayment exemption certificate issued for personal gain or to evade the prepayment of sales tax.

(f) Records. Adequate and complete records must be maintained by the seller and qualified retailer as evidence that the diesel fuel qualifies for the diesel fuel prepayment exemption.

(g) Operative Date. This regulation is operative as of October 9, 2002.

History—Adopted on September 24, 2003, effective January 21, 2004.

Amended February 24, 2015, effective July 1, 2015. In subdivision (a)(4), deleted the third paragraph which stated "Diesel fuel does not include the water in a diesel fuel and water emulsion of two immiscible liquids of diesel fuel and water, which emulsion contains an additive that causes the water droplets to remain suspended within the diesel fuel, provided the diesel fuel emulsion meets standards set by the California Air Resources Board." In the last paragraph of subdivision (b) replaced "entered on Form BOE 401GS line 10(e)(4) (Amount Subject" with "subject"; added "partial state tax exemption for" after "subject to the;" deleted "exemption )" after "processing"; and replaced "entered on line 14(a) (Transactions Subject to County Tax)" with "subject to county tax." The amendments also added section 60022 of the Revenue and Taxation Code as a reference.