Laws, Regulations, and Annotations

Lawguide Search

Business Taxes Law Guide—Revision 2026

Sales And Use Tax Regulations

Title 18. Public Revenues

Division 2. California Department of Tax and Fee Administration — Business Taxes

Chapter 4. Sales and Use Tax

Article 3. Manufacturers, Producers, Processors

Regulation 1534

Regulation 1534. Timber Harvesting Equipment and Machinery.

Reference: Section 6356.6, Revenue and Taxation Code.

(a) General. Commencing on and after September 1, 2001, section 6356.6 of the Revenue and Taxation Code partially exempts from sales and use tax the sale of, and the storage, use, or other consumption in this state, of off-road commercial timber harvesting equipment and machinery, and parts of off-road commercial timber harvesting equipment and machinery, that are purchased by a qualified person for use primarily in timber harvesting. The terms "off-road commercial timber harvesting equipment and machinery," "parts of off-road commercial timber harvesting equipment and machinery," "qualified person," and "commercial timber harvesting operations" are defined below.

For the period commencing on September 1, 2001, and ending on December 31, 2001, the partial exemption applies to the taxes imposed by sections 6051 and 6201 of the Revenue and Taxation Code (4.75%), but does not apply to the taxes imposed pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2002, and ending on June 30, 2004, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6201, and 6201.3 of the Revenue and Taxation Code (5%), but does not apply to the taxes imposed pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on July 1, 2004, and ending on March 31, 2009, the partial exemption applies to the taxes imposed by Sections 6051, 6051.3, 6051.5, 6201, 6201.3, and 6201.5 of the Revenue and Taxation Code (5.25%), but does not apply to the taxes imposed or administered pursuant to Sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or Section 35 of article XIII of the California Constitution.

For the period commencing on April 1, 2009, and ending on June 30, 2011, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6051.5, 6051.7, 6201, 6201.3, 6201.5, and 6201.7 of the Revenue and Taxation Code (6.25%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on July 1, 2011, and ending on December 31, 2012, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6051.5, 6201, 6201.3, and 6201.5 of the Revenue and Taxation Code (5.25%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2013, and ending on December 31, 2015, the partial exemption applies to the taxes imposed by section 36 of article XIII of the California Constitution and sections 6051, 6051.3, 6051.5, 6201, 6201.3, and 6201.5 of the Revenue and Taxation Code (5.50%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2016, and ending on December 31, 2016, the partial exemption applies to the taxes imposed by section 36 of article XIII of the California Constitution and sections 6051, 6051.3, 6201, and 6201.3 of the Revenue and Taxation Code (5.25%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

For the period commencing on January 1, 2017, the partial exemption applies to the taxes imposed by sections 6051, 6051.3, 6201, and 6201.3 of the Revenue and Taxation Code (5%), but does not apply to the taxes imposed or administered pursuant to sections 6051.2 and 6201.2 of the Revenue and Taxation Code, the Bradley-Burns Uniform Local Sales and Use Tax Law, the Transactions and Use Tax Law, or section 35 of article XIII of the California Constitution.

(b) Definitions. For purposes of this regulation:

(1) "Commercial timber harvesting operations" means the cutting or removal or both of timber or other solid wood forest products, from timberlands for commercial purposes, together with all the work incidental thereto, including but not limited to, construction and maintenance of roads, fuel breaks, firebreaks, stream crossings, landings, skid trails, beds for the falling of trees, fire hazard abatement, reforestation, and site preparation that involves disturbance of soil or burning of vegetation following timber harvesting activities. Such activities include, but are not limited to, bucking, bunching, chipping, debarking, delimbing, felling, forwarding, loading, piling, skidding, slashing, topping and yarding operations performed on timber. Commercial timber harvesting operations do not include the use of timber in processing activities or other activities resulting in the creation of other commercial wood products for sale to others, including, without limitation, milling, planing, carving, paper manufacturing, the treating of wood with creosote or other preservatives to prevent decay or protect against fire, or the packaging of wood chips for use in preparing food.

(2) "Off-road commercial timber harvesting equipment and machinery" means any new or used device, that may be powered by an internal combustion engine, electric motor, or otherwise, that is necessary in complying with any operational requirements of federal, state, or local government laws and regulations and is designed primarily for use off the highways, to propel, move, draw or cut timber in commercial timber harvesting operations. Such items include, but are not limited to, chainsaws, slashers, debarkers, harvesters, forwarders, feller-bunchers, cable yarding equipment, yarders, loading helicopters, chippers, bulldozers; loading equipment used to lift and move the equipment; graders; water trucks and similar logging road building and maintenance equipment; fuel storage equipment, site preparation equipment; all-terrain vehicles; fire fighting and safety equipment; timber harvest preparation equipment; reforestation tools and equipment; loaders; carriages; skidders; mobile metal spars; delimbers; chokers; steel cables; grapples; front-end loaders, and tractors or rubber tire skidders and other equipment used to fell, delimb, cross-cut, measure, sort, bunch, move and load timber for transport to roadside.

Off-road commercial timber harvesting equipment and machinery does not include junction boxes, switches, conduit and wiring, valves, pipes, tubing incorporated into fixed works, buildings, or other structures, whether or not such items are used solely or partially in connection with the operation of equipment and machinery. Off-road commercial timber harvesting equipment and machinery also does not include supplies such as articles of clothing, fuels, real property, materials or fixtures within the meaning of subdivisions (a)(4) and (a)(5), respectively, of Regulation 1521, Construction Contractors, including such items set forth in Appendix A and B of Regulation 1521.

(3) "Parts of off-road commercial timber harvesting equipment and machinery" means:

(A) All component parts and contrivances include, but are not limited to, belts, shafts, pipes, hoses and moving parts, that are parts of off-road commercial timber harvesting equipment and machinery as defined in subdivision (b)(2) that can be separated from the off-road commercial timber harvesting equipment and machinery and replaced. Parts of off-road commercial timber harvesting equipment and machinery do not include items that are consumed (e.g., burned, evaporate, dissolve, dissipate) through the regular use of the off-road commercial timber harvesting equipment and machinery (e.g., gasoline, cleaning agents, solutions, chemicals) which are ordinarily supplies; however, lubricants and fluids not consumed (e.g., engine oil not consumed as part of fuel for a two-stroke engine) is regarded as a component part.

(B) All repair and replacement parts for off-road commercial timber harvesting equipment and machinery as defined in subdivision (b)(2) which replace previous parts and can include parts that are identical to the parts they replace as well as parts that are different from the ones they replace, such as replacement parts added for the purpose of improving or modifying the off-road commercial timber harvesting equipment and machinery, whether purchased separately or in conjunction with a complete machine and regardless of whether the machine or component parts are assembled by a qualified person or another person. Parts of off-road commercial timber harvesting equipment and machinery do not include tangible personal property used in effectuating the repair of any timber harvesting equipment and machinery such as a wrench used to replace a spark plug, except tools used for repair that are designed exclusively for specific off-road commercial timber harvesting equipment and machinery.

(C) All equipment or devices used or required to operate, control, regulate, or maintain the machinery including, without limitation, computers, data processing equipment, and computer software, including both operating programs and application programs. Parts of off-road commercial timber harvesting equipment and machinery do not include tangible personal property used primarily in the administration, management, or marketing of timber harvesting operations.

(4) "Primarily" means used 50 percent or more of the time. As used herein, the qualified property has to be designed for use 50 percent or more of the time off-road in commercial timber harvesting operations and be used 50 percent or more of the time in timber harvesting.

(5) "Qualified person" means a person engaged in commercial timber harvesting operations. A qualified person is not required to be engaged 50 percent or more of the time in commercial timber harvesting operations.

(6) "Qualified property" means off-road commercial timber harvesting equipment and machinery, and the parts thereof, as defined in subdivisions (b)(2) and (b)(3) used primarily in timber harvesting.

(7) "Timber" means trees of any species maintained for eventual harvest for forest products or other forest purposes, whether planted or of natural growth, standing or down, including Christmas trees, on privately or publicly owned land, but does not mean nursery stock.

(8) "Timberland" means privately or publicly owned land which is devoted to and used for growing or timber harvesting, or for growing and timber harvesting and compatible uses, and which is capable of growing an average annual volume of wood fiber of at least 15 cubic feet per acre.

(c) Partial Exemption Certificates.

(1) In General. Qualified persons who purchase or lease qualified property from an in-state retailer, or an out-of state retailer obligated to collect use tax, must provide the retailer with a partial exemption certificate in order for the retailer to claim the partial exemption. If the retailer takes a partial exemption certificate timely and in good faith, as defined in subdivision (c)(5), from a qualified person, the partial exemption certificate relieves the retailer from the liability for the sales tax subject to exemption under this regulation or the duty of collecting the use tax subject to exemption under this regulation. A partial exemption certificate will be considered timely if it is taken any time before the retailer bills the purchaser for the qualified property, any time within the retailer's normal billing or payment cycle, any time at or prior to delivery of the qualified property to the purchaser, or no later than 15 days after the date of purchase. A partial exemption certificate that is not taken timely will not relieve the retailer of the liability for tax excluded by the partial exemption; however the retailer may present satisfactory evidence to the Board that the retailer sold the specific property to a qualified person and the property was primarily used in a qualifying manner. A partial exemption from the sales and use tax under this part shall not be allowed unless the retailer claims the partial exemption on its sales and use tax return for the reporting period during which the transaction subject to the partial exemption occurred. Where the retailer fails to claim the partial exemption as set forth above, the retailer may file a claim for refund as set forth in subdivision (e).

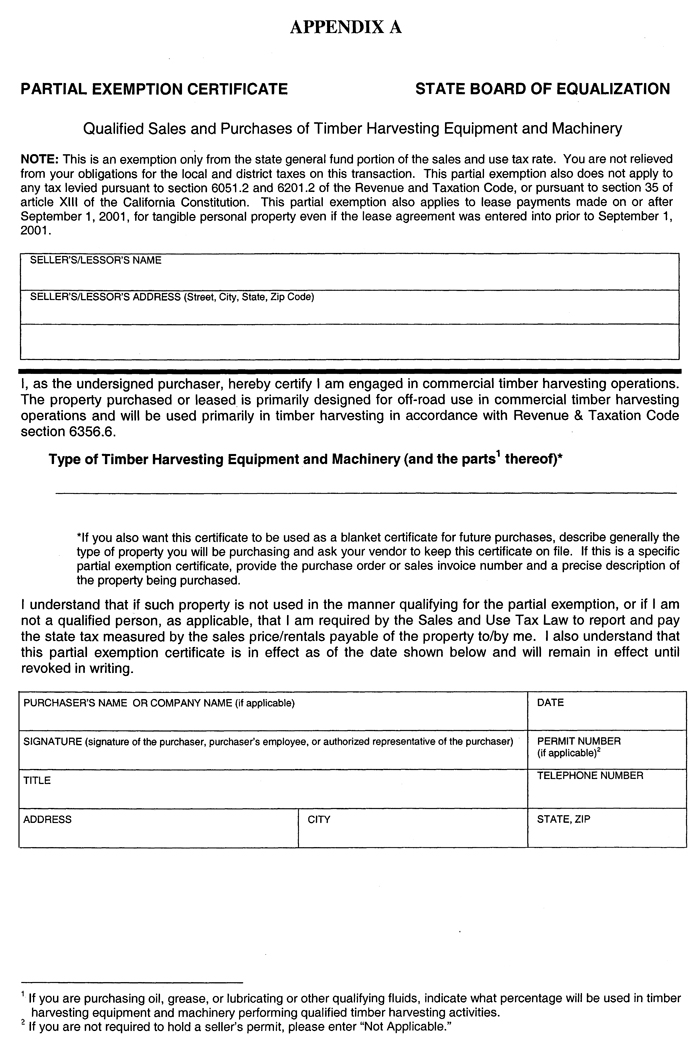

The partial exemption certificate form set forth in Appendix A may be used to claim the partial exemption.

(2) Blanket Partial Exemption Certificates. In lieu of requiring a partial exemption certificate for each transaction, a qualified person may issue a blanket partial exemption certificate. The partial exemption certificate form set forth in Appendix A may be used as a blanket partial exemption certificate. Appendix A may also be used as a specific partial exemption certificate if the purchaser provides the purchase order or sales invoice number and a precise description of the property being purchased. Qualified persons must include in the partial exemption certificate a description of the qualified property. If purchasing tangible personal property not qualifying for the partial exemption, the qualified person must clearly state in documents such as a written purchase order, sales agreement, lease, or contract that the sale or purchase is not subject to the blanket partial exemption certificate.

(3) Form of Partial Exemption Certificate. Any document, such as a letter or purchase order, timely provided by the purchaser to the seller will be regarded as a partial exemption certificate with respect to the sale or purchase of the property described in the document if it contains all of the following essential elements:

(A) The signature of the purchaser, purchaser's employee, or authorized representative of the purchaser.

(B) The name, address and telephone number of the purchaser.

(C) The number of the seller's permit held by the purchaser. If the purchaser is not required to hold a permit because the purchaser sells only property of a kind the retail sale of which is not taxable, e.g., food products for human consumption, or because the purchaser makes no sales in this state, the purchaser must include on the certificate a sufficient explanation as to the reason the purchaser is not required to hold a California seller's permit in lieu of a seller's permit number.

(D) A statement that the purchaser is engaged in commercial timber harvesting operations, and that the property purchased is primarily designed for off-road use in commercial timber harvesting operations and will be used primarily in timber harvesting.

(E) Description of property purchased.

(F) Date of execution of document.

(4) Retention and Availability of Partial Exemption Certificates. A retailer must retain each partial exemption certificate received from a qualified person for a period of not less than four years from the date on which the retailer claims a partial exemption based on the partial exemption certificate.

While the Board will not normally require the filing of the partial exemption certificate with a sales and use tax return, when necessary for the efficient administration of the Sales and Use Tax Law, the Board may on 30 days' written notice, require a retailer to commence filing with its sales and use tax returns copies of all partial exemption certificates. The Board may also require, within 45 days of the Board's request, retailers provide the Board access to any and all partial exemption certificates, or copies thereof, accepted for the purposes of supporting the partial exemption.

(5) Good Faith. A seller will be presumed to have taken a partial exemption certificate in good faith in the absence of evidence to the contrary. A seller, without knowledge to the contrary, may accept a partial exemption certificate in good faith where a qualified person states that he or she is engaged in commercial timber harvesting operations and states that the property purchased is primarily designed for off-road use in commercial timber harvesting operations and will be used primarily in timber harvesting. If the qualified person is buying property of a kind not normally used in timber harvesting, the seller should require a statement as to how the specific property purchased will be used. However, an exemption certificate cannot be accepted in good faith where the seller has knowledge that the property is not subject to a partial exemption, or will not be otherwise used in a partially exempt manner.

(d) Partial Exemption Certificate for Use Tax. The partial exemption certificate must be completed by a qualified person to claim a partial exemption from use tax on purchases of qualified property from an out-of-state retailer not obligated to collect the use tax. A partial exemption from the use tax shall not be allowed unless the purchaser or retailer claims the partial exemption on its individual use tax return, sales and use tax return, or consumer use tax return for the reporting period during which the transaction subject to the partial exemption occurred. Where the purchaser or retailer fails to claim the partial exemption as set forth above, the purchaser or retailer may file a claim for refund as set forth in subdivision (e).

The purchaser who files an individual use tax return must attach a completed partial exemption certificate to the return. The purchaser who is registered with the Board as a retailer or consumer and files a sales and use tax return or consumer use tax return must, within 45 days of the Board's request, provide the Board access to any and all documents that support the claimed partial exemption.

The partial exemption certificate form set forth in Appendix A may be used to claim the partial exemption.

(e) Refund of Partial Exemption.

(1) For the period commencing on September 1, 2001, and ending on June 30, 2002, a qualified person may claim the partial exemption on qualified purchases from an in-state retailer or an out-of-state retailer obligated to collect the use tax by furnishing the retailer with a partial exemption certificate on or before September 30, 2002. The retailer must refund the tax or tax reimbursement directly to the purchaser or, at the purchaser's sole option, the purchaser may be credited with such amount.

(2) A retailer who paid sales tax on a qualified sale or a person who paid use tax on a qualified purchase and who failed to claim the partial exemption as provided by this regulation may file a claim for refund equal to the amount of the partial exemption that he or she could have claimed pursuant to this regulation. The procedure for filing a claim shall be the same as for other claims for refund filed pursuant to Revenue and Taxation Code section 6901. For transactions subject to use tax, a qualified person filing a claim for refund of the partial exemption has the burden of establishing that he or she was entitled to claim the partial exemption with respect to the amount of refund claimed under this part. For transactions subject to sales tax, a person filing a claim for refund of the partial exemption has the burden of establishing that the purchaser of the qualified property otherwise met all the requirements of a qualified person at the time of the purchase subject to the refund claimed under this part.

(f) Improper Use of Partial Exemption.

(1) Property Used in a Manner Not Qualifying for the Partial Exemption. Notwithstanding subdivision (a), tax applies to any sale of, and the storage, use, or other consumption in this state of tangible personal property that is used in a manner not qualifying for the partial exemption under this regulation.

(2) Purchases by Non-qualified Persons. Notwithstanding subdivision (a), tax applies to any sale of, and the storage, use, or other consumption in this state of tangible personal property if a purchaser is not a qualified person.

(g) Purchaser's Liability for the Payment of Sales Tax.

(1) If a purchaser timely submits a copy of a partial exemption certificate to the retailer or partial exemption certificate for use tax to the Board, and then uses that tangible personal property in a manner not qualifying for the partial exemption, the purchaser shall be liable for payment of the sales tax, with applicable interest, to the same extent as if the purchaser were a retailer making a retail sale of the property at the time the property was so removed, converted, or used.

(2) A purchaser providing a partial exemption certificate accepted in good faith by the retailer or a partial exemption certificate for use tax to the Board for tangible personal property that does not qualify for the partial exemption is liable for payment of the sales tax, with applicable interest, to the same extent as if the purchaser were a retailer making a retail sale of the property at the time the property was purchased.

(h) Leases to Qualifying Persons.

(1) Leases—In General. Leases of tangible personal property which are classified as "continuing sales" and "continuing purchases" of tangible personal property, in accordance with Regulation 1660, "Leases of Tangible Personal Property—In General," may qualify for the partial exemption subject to all the limitations and conditions set forth in this regulation. This partial exemption may apply to rentals payable paid by a qualified person on or after September 1, 2001 with respect to a lease of qualified property to the qualified person, which qualified property is used primarily in timber harvesting, notwithstanding the fact that the lease was entered into prior to the effective date of this regulation. For purposes of this subdivision, a non-qualified person may purchase property for resale and subsequently lease the property to a qualified person subject to the partial exemption.

(2) Leases—Acquisition Sale and Leaseback. A qualified person will be regarded as having paid sales tax reimbursement or use tax with respect to that qualified person's purchase of property, within the meaning of those words as they are used in section 6010.65 of the Revenue and Taxation Code, if the qualified person has paid all applicable taxes with respect to the acquisition of the property, notwithstanding the fact that the sale and purchase of the property may have been subject to the partial exemption from tax provided by this regulation.

(3) Subsequent Lease of Property Acquired Subject to Partial Exemption. If a qualified person has acquired property subject to the partial exemption provided by this regulation and has paid all applicable taxes at that acquisition, the property will be regarded as property as to which sales tax reimbursement or use tax has been paid, and the subsequent lease of that property will not be subject to tax measured by rentals payable.

(i) Records. Adequate and complete records must be maintained by the qualified person as evidence that the qualified property purchased was primarily designed for off-road use in commercial timber harvesting operations and was used by the qualified person primarily in timber harvesting.

(j) Operative Date. This regulation is operative as of September 1, 2001.

History—Adopted June 19, 2002, operative September 1, 2001.

Amended June 30, 2004, effective August 18, 2004. Subdivision (a)—in 2nd unnumbered paragraph added phrase "and ending on June 30, 2004," added new third unnumbered paragraph to reflect the increase of the state portion of the sales and use tax to 5.25% on July 1, 2004.

Amended April 15, 2009, effective June 4, 2009. Amended subdivision (a) to reflect the increase in the partial exemption rate to 6.25% from April 1, 2009 until Revenue and Taxation Code sections 6051.7 and 6201.7 cease to be operative.

Amended effective January 9, 2012. Amended subdivision (a) to reflect the decrease in the partial exemption rate to 5.25% on July 1, 2011 caused by the expiration of sections 6051.7 and 6201.7 on June 30, 2011.

Amended March 13, 2013, effective July 11, 2013. Amended subdivision (a) to reflect the increase in the partial exemption rate to 5.50% on January 1, 2013 caused by the addition of section 36 to article XIII of the California Constitution.

Amended September 16, 2015, effective December 16, 2015. Amended subdivision (a) to reflect the one-quarter percent decrease in the partial exemption rate on January 1, 2016 caused by the expiration of Revenue and Taxation Code sections 6051.5 and 6201.5 on December 31, 2015.

Amended January 25, 2017, effective March 9, 2017. Amended subdivision (a) to reflect the one-quarter percent decrease in the partial exemption rate on January 1, 2017 caused by the expiration of the 0.25% sales and use tax imposed by section 36 of article XIII of the California Constitution.