Laws, Regulations, and Annotations

Lawguide Search

Business Taxes Law Guide—Revision 2026

Sales And Use Tax Regulations

Title 18. Public Revenues

Division 2. California Department of Tax and Fee Administration — Business Taxes

Chapter 4. Sales and Use Tax

Article 16. Resale Certificates; Demonstration, Gifts and Promotions

Regulation 1668

Regulation 1668. Sales for Resale.

Reference: Sections 6007, 6009.2, 6012.8, 6012.9, 6072, 6091–6095, 6241–6245, 6484, 6485, and 7153, Revenue and Taxation Code.

Automobile Dealers, effect of accepting from nondealer retailer, see Regulation 1566.

Construction Contractors, use by, see Regulation 1521.

Demonstration and Display, use of property purchased under resale certificates for, see Regulation 1669.

Drapery hardware installers accepting, see Regulation 1521.

Newspapers and Periodicals, for component parts of, see Regulation 1590.

Salt used by food processors, giving for, see Regulation 1525.

Vending machine operators furnishing, see Regulation 1574.

(a) Resale Certificate.

The burden of proving that a sale of tangible personal property is not at retail is upon the seller unless the seller timely takes in good faith a certificate from the purchaser that the property is purchased for resale. If timely taken in proper form as set forth in subdivision (b) and in good faith from a person who is engaged in the business of selling tangible personal property and who holds a California seller's permit as required by Regulation 1699, Permits, the certificate relieves the seller from liability for the sales tax and the duty of collecting the use tax. A certificate will be considered timely if it is taken at any time before the seller bills the purchaser for the property, or any time within the seller's normal billing and payment cycle, or any time at or prior to delivery of the property to the purchaser. A resale certificate remains in effect until revoked in writing.

(b) Form of Certificate.

(1) Any document, such as a letter or purchase order, timely provided by the purchaser to the seller will be regarded as a resale certificate with respect to the sale of the property described in the document if it contains all of the following essential elements:

(A) The signature of the purchaser, purchaser's employee or authorized representative of the purchaser.

(B) The name and address of the purchaser.

(C) The number of the seller's permit held by the purchaser. If the purchaser is not required to hold a permit because the purchaser sells only property of a kind the retail sale of which is not taxable, e.g., food products for human consumption, or because the purchaser makes no sales in this state, the purchaser must include on the certificate a sufficient explanation as to the reason the purchaser is not required to hold a California seller's permit in lieu of a seller's permit number.

(D) A statement that the property described in the document is purchased for resale. The document must contain the phrase "for resale." The use of phrases such as "non-taxable," "exempt," or similar terminology is not acceptable. The property to be purchased under the certificate must be described either by an itemized list of the particular property to be purchased for resale, or by a general description of the kind of property to be purchased for resale.

(E) Date of execution of document. (An otherwise valid resale certificate will not be considered invalid solely on the ground that it is undated.)

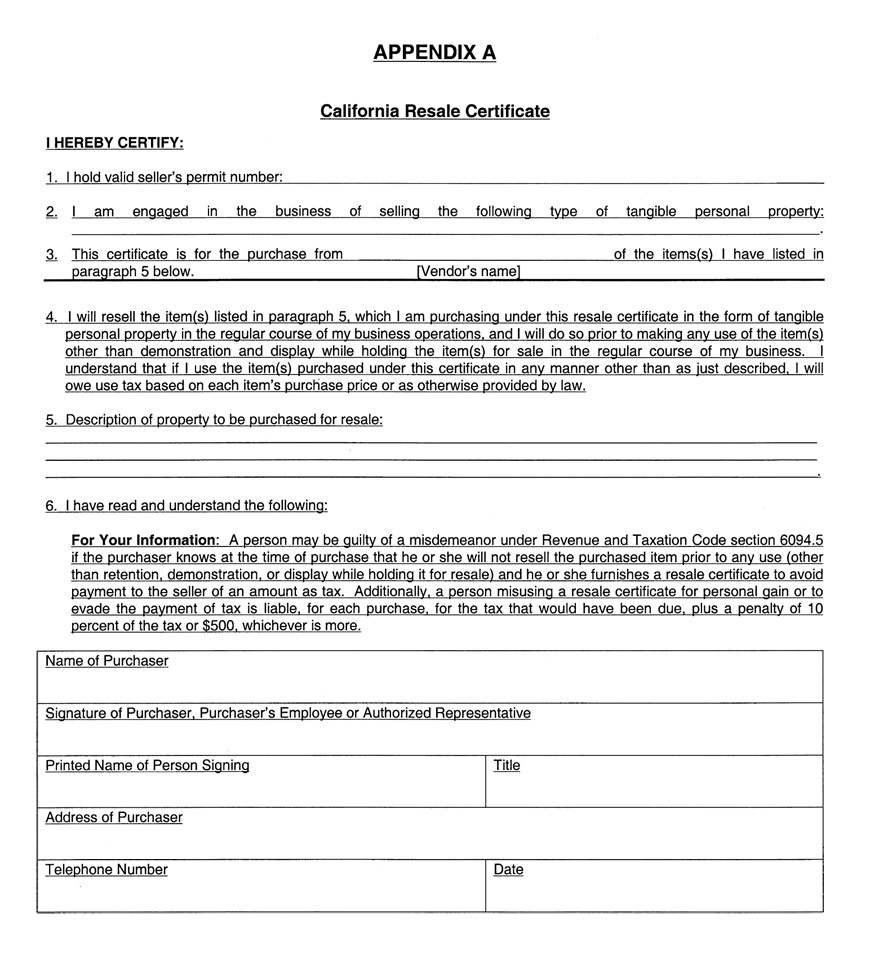

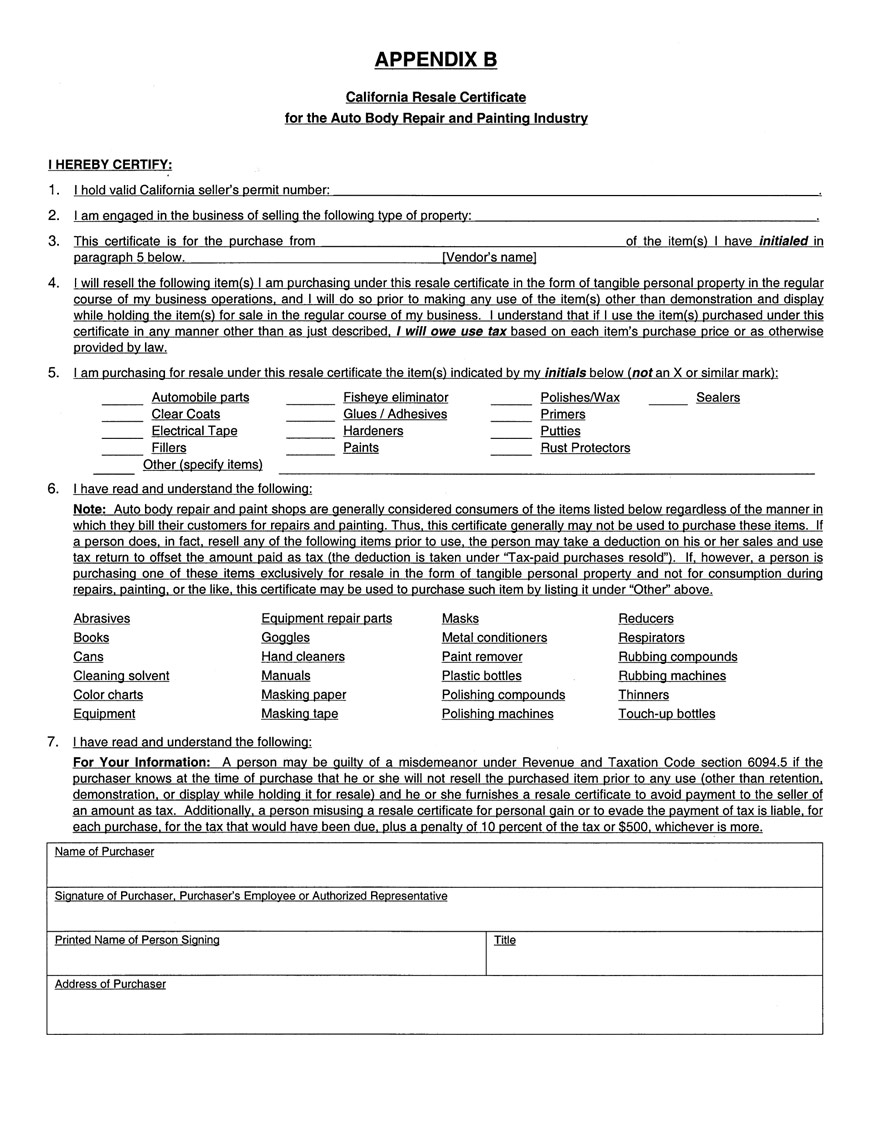

(2) A document containing the essential elements described in subdivision (b)(1) is the minimum form which will be regarded as a resale certificate. However, in order to preclude potential controversy, the seller should timely obtain from the purchaser a certificate substantially in the form shown in Appendix A of this regulation. If a purchaser operates an auto body repair and/or paint business, a specific resale certificate in substantially the same form as shown in Appendix B of this regulation should be used, rather than the general resale certificate shown in Appendix A.

(3) Blanket Resale Certificate. If a purchaser issues a general (blanket) resale certificate which provides a general description of the items to be purchased, and subsequently issues a purchase order which indicates that the transaction covered by the purchase order is taxable, the resale certificate does not apply with respect to that transaction. However, the purchaser will bear the burden of establishing either that the purchase order was sent to and received by the seller within the seller's billing cycle or prior to delivery of the property to the purchaser (whichever is the later), or that the tax or tax reimbursement was paid to the seller. The purchaser may avoid this burden by using the procedures described in subdivision (b)(4) below.

(4) Qualified Resale Certificate. If a purchaser wishes to designate on each purchase order whether the property being purchased is for resale, the seller should obtain a qualified resale certificate, i.e., one that states "see purchase order" in the space provided for a description of the property to be purchased. Each purchase order must then specify whether or not the property covered by the order is purchased for resale. The use of the phrases "for resale," "resale = yes," "nontaxable," "taxable = no," or similar terminology on a purchase order, indicating that tax or tax reimbursement should not be added to the sales invoice will be regarded as designating that the property described is purchased for resale provided the combination of the purchase order and the qualified resale certificate contains all the essential elements provided in subdivision (b)(1). However, a purchase order where the applicable amount of tax is shown as $0 or is left blank will not be accepted as designating that the property is purchased for resale, unless the purchase order also includes the phrase "for resale" or other terminology described above to specify that the property is purchased for resale. If each purchase order does not so specify, or is not issued timely within the meaning of subdivision (a), it will be presumed that the property covered by that purchase order was not purchased for resale and that sale or purchase is subject to tax. If the purchase order includes both items to be resold and items to be used, the purchase order must specify which items are purchased for resale and which items are purchased for use. For example, a purchase order issued for raw materials for resale and also for tooling used to process the raw materials should specify that the raw materials are purchased for resale and that the sale of the tooling is subject to tax.

The seller shall retain copies of the purchase orders along with the qualified resale certificates in order to support the sales for resale.

(5) If the seller does not timely obtain a resale certificate, the fact that the purchaser deletes the tax or tax reimbursement from the seller's billing, provides a seller's permit number to the seller, or informs the seller that the transaction is "not taxable" does not relieve the seller from liability for the tax nor from the burden of proving the sale was for resale.

(c) Good Faith. In absence of evidence to the contrary, a seller will be presumed to have taken a resale certificate in good faith if the resale certificate contains the essential elements as described in subdivision (b)(1) and otherwise appears to be valid on its face. If the purchaser insists that the purchaser is buying for resale property of a kind not normally resold in the purchaser's business, the seller should require a resale certificate containing a statement that the specific property is being purchased for resale in the regular course of business.

(d) Improper Use of Certificate. Except when a resale certificate is issued in accordance with subdivisions (h), (i) or (j):

(1) A purchaser, including any officer or employee of a corporation, is guilty of a misdemeanor punishable as provided in section 7153 if the purchaser, for the purpose of evading payment to the seller of tax or tax reimbursement, gives a resale certificate for property which the purchaser knows at the time of purchase will be used rather than resold.

(2) Any person, including any officer or employee of a corporation, who gives a resale certificate for property which he or she knows at the time of purchase is not to be resold by him or her or the corporation in the regular course of business is liable to the state for the amount of tax that would be due if he or she had not given such resale certificate. In addition to the tax, the person shall be liable to the state for a penalty of 10 percent of the tax or five hundred dollars ($500), whichever is greater, for each purchase made for personal gain or to evade the payment of taxes, as provided in sections 6072 and 6094.5.

(3) In addition to the penalty of 10 percent or five hundred dollars ($500), whichever is greater, if the person fails to report and pay the use tax due on the use of the property purchased improperly with a resale certificate, the person may be liable for the 10 percent penalty for negligence or the 25 percent penalty for fraud, as provided in sections 6484 and 6485.

(e) Other Evidence to Rebut Presumption of Taxability. A sale for resale is not subject to sales tax. A person who purchases property for resale and who subsequently uses the property owes tax on that use. A resale certificate which is not timely taken is not retroactive and will not relieve the seller of the liability for the tax. Consequently, if the seller does not timely obtain a resale certificate containing the essential elements as described in subdivision (b)(1), the seller will be relieved of liability for the tax only where the seller shows that the property:

(1) Was in fact resold by the purchaser and was not used by the purchaser for any purpose other than retention, demonstration, or display while holding it for sale in the regular course of business, or

(2) Is being held for resale by the purchaser and has not been used by the purchaser for any purpose other than retention, demonstration, or display while holding it for sale in the regular course of business, or

(3) Was consumed by the purchaser and tax was reported directly to the Board by the purchaser on the purchaser's sales and use tax return, or

(4) Was consumed by the purchaser and tax was paid to the Board by the purchaser pursuant to an assessment against or audit of the purchaser developed either on an actual basis or test basis.

(f) Use of XYZ Letters. A seller who does not timely obtain a resale certificate may use any verifiable method of establishing that it should be relieved of liability for tax under subdivision (e). One method that the Board authorizes to assist a seller in satisfying its burden to show that the sale was for resale or that tax was paid, is the use of "XYZ letters." XYZ letters are letters in a form approved by the Board which are sent to some or all of the seller's purchasers inquiring as to the purchaser's disposition of the property purchased from the seller. An XYZ letter will include certain information and request responses to certain questions, set forth below. The XYZ letter may also be further customized by agreement between the Board's staff and the seller to reflect the seller's particular circumstances.

(1) An XYZ letter may include the following information: seller's name and permit number, date of invoice(s), invoice number(s), purchase order number(s), amount of purchase(s), and a description of the property purchased or other identifying information. A copy of the actual invoice(s) may be attached to the XYZ letter. The XYZ letter will request the purchaser to complete the statement and include the purchaser's name, seller's permit number and nature of the purchaser's business. The statement shall be signed by the purchaser, purchaser's employee or authorized representative, and include the printed name of the person signing the certificate, title, date, telephone number and city.

(2) An XYZ letter will request that the purchaser, purchaser's employee or authorized representative check one of the boxes provided inquiring as to whether the property in question was:

(A) Purchased for resale and resold in the form of tangible personal property, without any use other than retention, demonstration, or display while being held for sale in the regular course of business;

(B) Purchased for resale and presently in resale inventory, without having been used for any purpose other than retention, demonstration, or display while being held for sale in the regular course of business;

(C) Purchased solely for leasing and was so leased. Tax has been paid directly to the Board measured by the purchase price or rental receipts ("tangible personal property"); or tax has been paid measured by the purchase price or fair rental value ("mobile transportation equipment");

(D) Purchased for resale but consumed or used (whether or not subsequently resold); or

(E) Purchased for use.

(F) When the purchaser answers either (D) or (E) affirmatively (box checked), the XYZ letter will inquire further whether:

1. The tax was paid directly to the Board on the purchaser's Sales and Use Tax Return, and if so, in what amount;

2. The tax was added to the billing of the seller and remitted to the seller, and if so, in what amount;

3. The tax was paid directly to the Board by the purchaser pursuant to an assessment against or audit of the purchaser developed either on an actual basis or test basis; or

4. The purchaser confirms that the purchase is a taxable transaction and that tax is applicable.

(3) A response to an XYZ letter is not equivalent to a timely and valid resale certificate. A purchaser responding affirmatively to questions reflected in paragraphs (A), (B), (C), or (D) of subdivision (f)(2) will be regarded as confirming the seller's belief that a sale was for resale for purposes of subdivision (g). However, the Board is not required to relieve a seller from liability for sales tax or use tax collection based on a response to an XYZ letter. The Board may, in its discretion, verify the information provided in the response to the XYZ letter, including making additional contact with the purchaser or other persons to determine whether the purchase was for resale or for use, or whether tax was paid by the purchaser. When the Board accepts the purchaser's response to an XYZ letter as a valid response, the Board shall relieve the seller of liability for sales tax or use tax collection.

(4) When there is no response to an XYZ letter, the Board staff should consider whether it is appropriate to use an alternative method to ascertain whether the seller should be relieved of tax under subdivision (e) with respect to the questioned or unsupported transaction(s).

(g) Purchaser's Liability for Tax. A purchaser who issues a resale certificate containing the essential elements as described in subdivision (b)(1) and that otherwise appears valid on its face, or who otherwise purchases tangible personal property that is accepted by the Board as purchased for resale pursuant to subdivision (f) and who thereafter makes any storage or use of the property other than retention, demonstration, or display while holding it for sale in the regular course of business is liable for use tax on the cost of the property. The tax is due at the time the property is first stored or used and must be reported and paid by the purchaser with the purchaser's tax return for the period in which the property is first so stored or used. A purchaser cannot retroactively rescind or revoke a resale certificate and thereby cause the transaction to be subject to sales tax rather than use tax.

A purchaser who issues a resale certificate for property which the purchaser knows at the time of purchase is not to be resold in the regular course of business is liable for the sales tax on that purchase measured by the gross receipts from the sale to that purchaser. The tax is due as of the time the property was sold to the purchaser and must be reported and paid by the purchaser with the purchaser's tax return for the period in which the property was sold to the purchaser.

(h) Mobilehomes. A mobilehome retailer who purchases a new mobilehome for sale to a customer for installation for occupancy as a residence on a foundation system pursuant to section 18551 of the Health and Safety Code, or for installation for occupancy as a residence pursuant to section 18613 of the Health and Safety Code, and which mobilehome is thereafter subject to property taxation, may issue a resale certificate to the mobilehome vendor even though the retailer is classified as a consumer of the mobilehome by sections 6012.8 and 6012.9 of the Revenue and Taxation Code. Also, a mobilehome retailer, licensed as a mobilehome dealer under section 18002.6 of the Health and Safety Code, who purchases a new mobilehome for sale to a customer for installation for occupancy as a residence on a foundation system pursuant to section 18551 of the Health and Safety Code, may issue a resale certificate to the mobilehome vendor even though the mobilehome retailer may have the mobilehome installed on a foundation system as an improvement to realty prior to the retailer's sale of the mobilehome to the customer for occupancy as a residence.

Where the mobilehome is acquired by a mobilehome retailer, who is not licensed as a dealer pursuant to section 18002.6 of the Health and Safety Code, for affixation by the retailer to a permanent foundation, or for other use or consumption (except demonstration or display while holding for sale in the regular course of business), prior to sale, the mobilehome retailer may not issue a resale certificate. The mobilehome retailer shall notify the vendor that the purchase is for consumption and not for resale. When a mobilehome manufacturer or other vendor is informed or has knowledge that the purchaser will install the mobilehome on a permanent foundation prior to its resale, the manufacturer or other vendor is not making a sale for resale. Such vendor is making a taxable retail sale and cannot accept a resale certificate in good faith.

(i) Mobile Transportation Equipment. Any person, other than a person exempt from use tax, such as under Revenue and Taxation Code section 6352, who purchases mobile transportation equipment for the sole purpose of leasing that equipment, may issue a resale certificate for the limited purpose of reporting use tax based on fair rental value as provided in Regulation 1661.

(j) Counterfeit Goods. A sale of tangible personal property with a counterfeit mark on, or in connection with, that sale by a convicted seller is included in the definition of "retail sale" per Revenue and Taxation Code section 6007, and therefore taxable. "Storage" and "use" as defined in Revenue and Taxation Code section 6009.2, includes any purchase of tangible personal property with a counterfeit mark on, or in connection with, that purchase by a convicted purchaser and is subject to tax. This is regardless of whether the counterfeit goods were sold for resale or held with the intent to be resold. A "counterfeit mark" is a spurious mark that is used in a manner described in section 2320 of title 18 of the United States Code.

History—Effective July 1, 1939.

Adopted as of January 1, 1945, as a restatement of previous rulings.

Amended June 20, 1967, effective July 1, 1967.

Amended and renumbered November 3, 1969, effective December 5, 1969.

Amended April 6, 1977, effective July 1, 1977. Added new method of proof for resale, detailed what is adequate proof for resale, and clarified effect of purchase for use on a resale certificate.

Amended December 7, 1977, effective January 19, 1978. In (e) added the tax that would be due.

Amended July 28, 1982, effective June 26, 1983. Added new (e) and (f), renumbered (g) and (h), and added reference to Section 6072 to (g).

Amended April 9, 1985, effective June 27, 1985. In subdivision (g), amended to specify that the penalty provisions are also applicable to any officer or employee of a corporation who gives a resale certificate for property which he or she knows at the time of purchase will be used rather than resold. Added a reference to Section 6094.5 of the Revenue and Taxation Code with respect to the type of penalties a purchaser may be liable for if the purchaser makes an improper use of a resale certificate. Deleted subdivision (h) since it pertained to the effective date of amendments to the regulation which occurred in 1977.

Amended April 9, 1986, effective July 5, 1986. In subdivision (e), amended explanation under which mobilehome retailers may issue resale certificates to mobilehome vendors.

Amended March 28, 2001, effective July 6, 2001. Subdivision (b)(2)—The paragraph labeled "For Your Information" was added to the sample Resale Certificate currently in the regulation. A new paragraph was added providing a cross-reference to the resale certificate for the auto body repair and painting industry and the new certificate was added.

Amended December 20, 2001, effective May 17, 2002. Regulation re-titled "Sales for Resale." Word "subsection" replaced with "subdivision" throughout. Subdivision (a): re-titled "Resale Certificate; subdivision (a)(2) deleted and its language transferred to new subdivision (g) and expanded; designation (a)(1) deleted and its language transferred to subdivision (a) and rewritten. Subdivision (b): subdivision (b)(1)(A) words "or an agent or" deleted and words "purchaser's" and "authorized representative" added; subdivision (b)(1)(c) comma after word "purchaser" replaced by a period and word "or" deleted in first sentence; phrase "an … number." replaced with phrase "the … number." at the end of the subdivision. Subdivision (b)(1)(D)—new third sentence added. Subdivision (b)(2)—word "paragraph" added to first sentence and word "following" deleted from second sentence with new phrase "shown … regulation" and new third sentence added and sample resale certificates moved to new Appendices A and B. Subdivision (b)(3)—phrase "within … later)" added to second sentence. Subdivision (b)(4) word "that" replaced with "whether" in the first sentence; phrase "or … (a)" added to third sentence. Subdivision (c) deleted and its language transferred to new subdivision (e) with new fourth sub-paragraph added. Subdivision (d) re-designated (c) accordingly. Phrase "In … contrary," transferred to beginning of first sentence and capitalized and letter "A" changed to lower case, and phrase "if … face" added. New subdivisions (d)–(g) added. Former subdivision (e) re-designated (h) accordingly. Former subdivision (f) re-designated (i), accordingly; language "person … equipment" replaced with "person … 1661." Former subdivision (g) deleted.

Amended February 1, 2007, effective June 5, 2007. Amended subdivision (d) to clarify the penalties that may be applied for improper use of a resale certificate.

Amended May 27, 2009, effective August 29, 2009. Added titles to subdivisions (b)(3) and (b)(4). Amended subdivision (b)(4) to clarify the proper use of a qualified resale certificate. In subdivision (b)(2), changed "paragraph (1) above" to "subdivision (b)(1)," and in subdivisions (c) and (e), changed "(b)(1)" to "subdivision (b)(1)" to enhance consistency throughout the regulation.

Amended February 23, 2016, effective July 1, 2016. In subdivision (d) replaced "subdivision (h) or (i)" with "subdivisions (h), (i) or (j)" inserted "to show" between "burden" and "that" in subdivision (f); replaced the period with "; or" at the end of subdivision (f)(2)(F)3. In subdivision (h) replaced "Section" with "section" and "Sections" with "sections" throughout; deleted "effective September 19, 1985," from before "a mobilehome retailer" in the second sentence in subdivision (h); added new subdivision (j); and added references to Revenue and Taxation Code sections 6007 and 6009.2 to the reference note.

Note.—See Business Taxes General Bulletin 61-2 following Regulation 1525.