Laws, Regulations, and Annotations

Lawguide Search

Business Taxes Law Guide—Revision 2026

Sales And Use Tax Regulations

Title 18. Public Revenues

Division 2. California Department of Tax and Fee Administration — Business Taxes

Chapter 4. Sales and Use Tax

Article 7. Specific Kinds of Property and Exemptions Generally

- 1584 Membership Fees

- 1585 Cellular Telephones, Pagers, and Other Wireless Telecommunication Devices

- 1586 Works of Art and Museum Pieces for Public Display

- 1587 Animal Life, Feed, Drugs and Medicines

- 1588 Seeds, Plants and Fertilizer

- 1589 Containers and Labels

- 1590 Newspapers and Periodicals

- 1591 Medicines and Medical Devices

- 1591.1 Specific Medical Devices, Appliances, and Related Supplies

- 1591.2 Wheelchairs, Crutches, Canes, and Walkers

- 1591.3 Vehicles for Physically Handicapped Persons

- 1591.4 Medical Oxygen Delivery Systems

- 1592 Eyeglasses and Other Ophthalmic Materials

- 1593 Aircraft and Aircraft Parts

- 1594 Watercraft

- 1595 Occasional Sales—Sale of a Business—Business Reorganization

- 1596 Buildings and Other Property Affixed to Realty

- 1597 Property Transferred or Sold by Certain Nonprofit Organizations

- 1598 Motor Vehicle and Aircraft Fuels

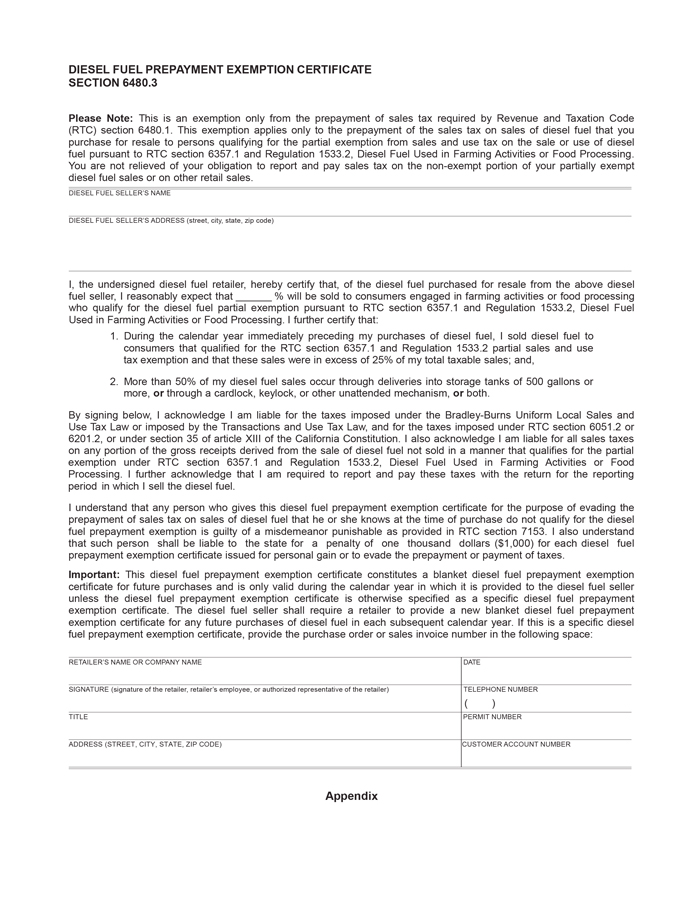

- 1598.1 Diesel Fuel Prepayment Exemption

- 1599 Coins and Bullion

Regulation 1584. Membership Fees.

Reference: Sections 6011.1, 6012, and 6012.1, Revenue and Taxation Code.

(a) Application of Tax.

(1) In General. Membership fees related to the anticipated retail sale of tangible personal property are includible in taxable gross receipts when either

(A) the retailer sells its products only to members and the membership fee exceeds a nominal amount,

or

(B) regardless of the amount of the membership fee, the retailer sells its products for a lower price to a person who has paid the membership fee than to a person who has not paid the fee.

(2) The membership fees described in subdivision (a)(1)(A) or (a)(1)(B) are part of the gross receipts of the person selling tangible personal property to a member. It is immaterial that the person who sold the membership is not the person who sells the tangible personal property to a member. Any sale of a membership described in subdivision (a)(1)(A) or (a)(1)(B) is regarded as related to the retail sale by the retailer selling tangible personal property to a member, not by the person selling the membership, measured by the amounts received by the person selling the membership.

(3) Incidental Sales. Charges for membership fees not related to anticipated retail transactions are not subject to tax. For example, when a country club or similar organization charges fees (dues) to members and provides substantial service benefits, e.g., the use of golfing, tennis and swimming facilities, the membership fees are not related to sales even though the organization may establish minimum meal and drink purchase requirements for its members.

(4) Consumer Cooperatives. Initial or periodic membership fees received by consumer cooperatives, as defined in sections 6011.1 and 6012.1 of the Revenue and Taxation Code, are not subject to tax.

(b) Nominal Amount.

(1) For purposes of this regulation, beginning January 1, 2021, the term "nominal amount" means an amount totaling $70 or less per year subject to increase as provided in subdivision (b)(2). For periods from January 1, 2016, through December 31, 2020, the term "nominal amount" for purposes of this regulation means an amount totaling $60 or less per year. For periods from January 1, 2011 through December 31, 2015, the term "nominal amount" for purposes of this regulation means an amount totaling $55 or less per year. For periods from January 1, 2006 through December 31, 2010, the term "nominal amount" for purposes of this regulation means an amount totaling $50 or less per year. For periods from January 1, 2001 through December 31, 2005, the term "nominal amount" for purposes of this regulation means an amount totaling $45 or less per year. For periods prior to January 1, 2001, the term "nominal amount" for purposes of this regulation meant an amount totaling $40 or less per year. Amounts received for memberships which are in conjunction with a basic membership (add-ons) are not considered a part of the basic membership fee in determining the nominal amount of the basic membership. Additional cards issued under the same membership number are sales of separate memberships.

(2) During September in the year 2000, and every five years thereafter, the threshold for the nominal amount will be adjusted effective the following January 1, rounded to the nearest $5, to reflect changes in the California Consumer Price Index (CCPI) whenever that change is more than 5 percent higher than any previous adjustment. For purposes of computing the CCPI increase, the June 30 CCPI index of the computation year will be compared with the June 30 CCPI index of the computation year which resulted in an adjusted nominal amount. For example, for the January 1, 2026 adjustment computation, the CCPI index on June 30, 2025, will be compared with the CCPI index on June 30, 2020. If no adjustment is made at that time, the next comparison will be of the CCPI index on June 30, 2030 with the CCPI index on June 30, 2020.

History—Adopted February 22, 1996, effective August 2, 1996.

Amended October 31, 2000, effective January 1, 2001. Subdivision (b)(1)—phrase "beginning January 1, 2001" added; number $40 replaced with $45 in first sentence; Phrase "For periods … per year" added in second sentence. Subdivision (b)(2)—"2006" replaced "2001," "2000" replaced "1995," and "2010" replaced "2005."

Amended May 25, 2004, effective August 26, 2004. New subdivision (a)(2) added. Current subdivisions (a)(2) and (3) re-numbered (a)(3) and (4) accordingly.

Amended October 25, 2005, effective January 10, 2006. Adjusted the "nominal amount" in subdivision (b)(1) from $45 to $50 or less per year, operative January 1, 2006, to reflect an increase in the California Consumer Price Index as provided in the regulation. In subdivision (b)(2), updated the example years.

Amended March 25, 2010, effective May 13, 2010. Subdivision (c) deleted to remove unnecessary effective date.

Amended November 16, 2010, effective January 12, 2011. Adjusted the "nominal amount" in subdivision (b)(1) from $50 to $55 or less per year, operative January 1, 2011, to reflect an increase in the California Consumer Price Index as provided in the regulation. In subdivision (b)(2), updated the example years.

Amended September 16, 2015, effective December 8, 2015. Adjusted the "nominal amount" in subdivision (b)(1) from $55 to $60 or less per year, operative January 1, 2016, to reflect an increase in the California Consumer Price Index as provided in the regulation. In subdivision (b)(2), updated the example years.

Amendments filed with the Secretary of State May 25, 2021, and effective May 25, 2021. The amendments adjusted the "nominal amount" in subdivision (b)(1) from $60 to $70 or less per year, operative January 1, 2021, to reflect an increase in the California Consumer Price Index as provided in the regulation. In subdivision (b)(2), updated the example years.

Regulation 1585. Cellular Telephones, Pagers, and Other Wireless Telecommunication Devices.

Reference: Sections 6006, 6010, 6011, 6012, and 6055, Revenue and Taxation Code.

(a) Definitions.

(1) Wireless Telecommunication Device. A portable communication device such as a wireless telephone or pager requiring activation by a wireless telecommunications service provider or seller of utility services in order to send, receive, or send and receive transmissions via a network of wireless transmitters throughout multiple service areas, or otherwise. The term includes devices based on analog technology and devices based on digital technology.

(2) Wireless Telecommunications Service Provider. A utility regulated by the Public Utilities Commission or the Federal Communications Commission which offers or provides wireless communication or paging services.

(3) Bundled Transaction. The retail sale of a wireless telecommunication device which contractually requires the retailer's customer to activate or contract with a wireless telecommunications service provider for utility service for a period greater than one month as a condition of that sale. A transaction is a bundled transaction within the meaning of this regulation without regard to the method in which the price is stated to the customer. Also, it is immaterial whether the wireless telecommunication device and utility service are sold for a single price or are separately itemized in the context of a sale or on a sales invoice. A transaction is a bundled transaction if goods and services are sold as a single package, whether wireless telecommunication service is supplied to the customer by the retailer or by an independent service supplier. In such transactions, wireless devices may be sold at a "discounted" price, as an inducement for the customer to enter into an extended service contract. The fact that a wireless telecommunication device, such as a PCS (Personal Communication Service) telephone, may, because of its technological specifications, be subject to activation with only one service supplier, does not alone mean that the sale of the device will be treated as a bundled transaction.

(4) Unbundled Sales Price. The price at which the retailer has sold specific wireless telecommunication devices to customers who are not required to activate or contract for utility service with the retailer or with an independent wireless telecommunications service provider for utility service as a condition of that sale. If the retailer cannot establish an unbundled sales price to the satisfaction of the Board based upon its own sales records, the unbundled sales price of the device shall equal the fair retail selling price of that device. If tax is reported and paid on an amount equal to the cost of the device plus a markup on cost of at least 18 percent, such amount shall be regarded as the fair retail selling price of the device. The unbundled sales price of an obsolete wireless telecommunication device shall equal the actual selling price of that device.

(b) Application of Tax.

(1) In General. Tax applies to the gross receipts from the retail sale of a wireless telecommunication device. The retailer of the wireless telecommunication device is required to report and pay the tax.

(2) Unbundled Transactions. Tax applies to the gross receipts from the retail sale of a wireless telecommunication device prior to October 1, 1995, or sold in a transaction not described in subdivisions (a)(3), (b)(5), or (b)(6), measured by the actual gross receipts received by the retailer from the end-use customer from the sale of that device.

(3) Bundled Transactions. Tax applies to the gross receipts from the retail sale of a wireless telecommunication device sold in a bundled transaction, measured by the unbundled sales price of that device. Tax applies to the unbundled sales price whether the wireless telecommunication device and utility service are sold for a single price or are separately itemized in the context of a sale or on a sales invoice. The retailer of the wireless telecommunication device is required to report and pay tax measured by the unbundled sales price of the device and may collect tax or tax reimbursement from its customer measured by the unbundled sales price. Tax does not apply to the charges in excess of the unbundled sales price made for telecommunication services.

(4) Activation Fees. Tax does not apply to a one-time charge for activating a new wireless telecommunication device with, or on behalf of, a wireless telecommunications service provider where the charge is separately stated and is not for the electronic or physical modification of the device in order for it to function within a wireless telecommunications service provider's service network. A one-time charge for activating a wireless telecommunication device is subject to tax if the activation consists of the physical or electronic modification or fabrication of a wireless telecommunication device in order for the device to function within a wireless telecommunications service provider's service network. The person collecting this fee is required to report and pay tax on that amount. Any subsequent charge for the physical or electronic modification or fabrication of that device which changes the customer's telephone number or which allows that customer to utilize a different wireless telecommunications service provider is subject to tax as set forth in Regulation 1546 (18 CCR 1546).

For purposes of this subdivision, "physical or electronic modification or fabrication of a wireless telecommunication device" does not include the manual input of activation information into the device solely by means of the device's own numeric or function keys, nor does it include the remote electronic input of activation information into the device.

(5) Consignment Transactions and Sale or Return Transactions. In transactions of this type, a service provider furnishes an inventory of wireless telecommunication devices to an independent retailer without charge or at a nominal price. The independent retailer sells the devices to end-use customers, retaining the proceeds of sale. The end-use customer must contract for wireless service for a period greater than one month with the wireless service provider or, if the end-use customer does not enter such an extended service contract, the end-use customer is required to pay additional service consideration for the device to the service provider. Typically, a credit card imprint is taken by the retailer, to the benefit of the service provider, at the time of the sale, to guarantee payment of the additional consideration. This is a bundled transaction in which the measure of tax is the unbundled sales price. The service provider may collect sales tax reimbursement from the end-use customer. The nominal amount collected from the end-use customer is in the nature of a commission and is not subject to tax. The person providing the device to the end-use customer may not collect sales tax reimbursement from the end-use customer.

(6) Sales at Less Than 50 Percent of Cost. Operative January 1, 1999, except with respect to transfers described in (b)(5), any person making any sale, whether at retail or for resale, in a bundled transaction or otherwise, of a wireless telecommunication device at a price, measured by the actual sales price in an unbundled transaction or the unbundled sales price, as determined under this regulation, in a bundled transaction, less than 50 percent of cost, must report and pay use tax measured by the cost to it of the device. If the sale at less than 50 percent of cost is a retail sale, sales tax does not apply to that retail sale. The person making the sale of the device is the consumer of the device for sales and use tax purposes and may not collect tax reimbursement from its customer. Likewise, persons who sell devices for resale at less than 50 percent of cost are consumers. They must report and pay use tax measured by the cost to them of the device. In this case, any subsequent retail sale of the device is subject to sales tax unless that sale is at less than 50 percent of cost. Sales tax reimbursement may be collected from the end-use customer based upon the retail selling price of the device to the end-use customer. This subdivision shall not, however, be applicable in any instance involving the sale of a functionally or economically obsolete wireless telecommunication device.

(c) Bad Debt Deductions.

(1) In General. The provisions of Regulation 1642, "Bad Debts" (18 CCR 1642), apply to retailers making sales of wireless telecommunication devices pursuant to subdivision (b)(1).

(2) Charge-Backs To The Retailer. Retailers reporting tax measured by the unbundled sales price of a wireless telecommunication device may take a bad debt deduction pursuant to Regulation 1642 when a payment or rebate from a wireless telecommunications service provider is charged-back to the retailer based on a customer's termination of its contract with the wireless telecommunications service provider before the date specified in the utility service contract. The amount of bad debt deduction claimed by a retailer may not exceed the difference between the gross receipts on which tax was reported and paid by the retailer, and the total amount collected and retained by the retailer from the sale of the wireless telecommunication device excluding any amounts collected from the customer as tax or tax reimbursement. Any tax or tax reimbursement collected by the retailer on the amount of bad debt deduction claimed by the retailer constitutes excess tax reimbursement and must be returned to the customer or paid to the Board unless the customer and retailer agree that this amount may be applied toward the amounts owed by the customer on the debt. The customer and retailer will be regarded as having agreed to the application of any excess tax reimbursement to the customer's debt where the retailer's books reflect both the debt owed by the customer and the corresponding credit for excess tax reimbursement.

History—Adopted October 15, 1998, effective February 11, 1999.

Regulation 1586. Works of Art and Museum Pieces for Public Display.

Reference: Sections 6365 and 6366.3, Revenue and Taxation Code.

(a) General.

(1) Original Work of Art. Tangible personal property which is an original work of art and which is purchased by or for donation to certain public or nonprofit organizations for the purpose of display to the public in museums or public places is exempt from the sales and use taxes under certain conditions.

(2) Museum Pieces. Tangible personal property purchased by certain organizations to replace museum pieces which were destroyed by a calamity are exempt from the sales and use taxes under certain conditions.

(b) Definitions.

(1) "Original Work of Art" for purposes of this regulation means tangible personal property which has been created as a unique object intended to provide aesthetic pleasure to the beholder and/or to express the emotions of the artist. The form in which an original work of art is presented includes but is not limited to:

(A) visual art, e.g., a drawing, painting, mural, fresco, sculpture, mosaic, film, or photograph, a work of calligraphy, a work of graphic art (an etching, lithograph, offset print, silk screen, or a work of graphic art of like nature),

(B) crafts, e.g., crafts in clay, textile, fiber, wood, metal, plastic, glass, costume, dress, clothing, personal adornment, and like materials, or

(C) mixed media, e.g., a collage, assemblage, or any combination of the foregoing art media.

(2) "Museum" for purposes of this regulation means a place specifically designated for display of artifacts or objects of art which either:

(A) has a significant portion of its display space open to the public without charge during its normal operating hours;

(B) has its entire display space open to the public without charge for at least six of its normal operating hours during each month of operation; or

(C) has its entire display space open without charge to a segment of the student or adult population for educational purposes.

(c) Application of Tax.

(1) Original Works of Art.

(A) Tax does not apply to the sale or use of original works of art which are:

1. purchased by this state, or any city, county, city and county, or other local governmental entity in this state;

2. purchased by any nonprofit organization which operates a public museum under contract for such governmental entity;

3. purchased by any nonprofit organization qualifying for exemption from state income tax pursuant to section 23701d of the Revenue and Taxation Code. The works of art must be purchased for display in a museum either operated by the purchaser or by another nonprofit organization which qualified for exemption pursuant to section 23701d. The museum in which the art is displayed must be open to the public regularly for not less than 20 hours per week and for not less than 35 weeks of the calendar year;

4. purchased by any person for donation to the above governmental entities or nonprofit organizations. To qualify for exemption from the tax under this subparagraph, donated works of art must be delivered by the retailer of the art directly to the donee pursuant to the instructions of the buyer-donor. Written evidence of transfer of title to the works of art from the buyer-donor to the donee must be maintained by the retailer and the buyer-donor to support the exemption; or

5. operative January 1, 2007, leased from one nonprofit organization to another nonprofit organization for 35 years or more, if both lessor and lessee are nonprofit organizations as defined in subdivisions (c)(1)(A)(2) and (c)(1)(A)(3) of this regulation.

(B) The exemption provided by subdivision (c)(1)(A) applies only to original works of art which are purchased or leased to become part of the permanent collection of any of the following:

1. a museum;

2. a nonprofit corporation which (1) has qualified for exemption from the state income tax pursuant to Revenue and Taxation Code section 23701d, (2) regularly loans not less than 85 percent of the value of its collection of works of art to one or more museums, and (3) is required by its articles of incorporation to loan its works of art and is otherwise prohibited by its articles from making any private use of its works of art. The works of art for which the exemption is claimed pursuant to this subparagraph must be placed on display at a museum in California for not less than 24 months during the three-year period commencing from the date of purchase; or

3. operative January 1, 1988, this state and any city, county, city and county, or other local governmental entity in this state for display to the public in buildings, parks, plazas, or other places which are open to the public without charge for not less than 20 hours per week and for not less than 35 weeks of the calendar year.

Operative January 1, 2007, "permanent collection" as it applies to leases of original works of art, means a collection with a lease term of 35 years or more.

(2) Museum Pieces.

(A) Tangible personal property is exempt from the sales and use tax if purchased to replace destroyed objects of a museum's permanent collection when such property is purchased by:

1. a nonprofit museum regularly open to the public and operated by or for a local or state government entity,

2. a nonprofit museum regularly open to the public and operated by a nonprofit organization which has qualified for exemption from the state income tax pursuant to section 27301d of the Revenue and Taxation Code, or

3. operative January 1, 1988, this state or any local governmental entity in this state as part of a public art collection for display in a space which is open to the public without charge.

(B) To qualify for the exemption, the property must be purchased and used exclusively for display purposes. However, the property purchased does not need to be similar in character to the property it is replacing. The exemption does not extend to display cases, shelving, lamps, lighting fixtures, or other items of tangible personal property utilized in the operations of the museum. The purchased property must be:

1. purchased to replace property which has been physically destroyed by fire, flood, earthquake, or other calamity,

2. purchased within three years from the date of the calamity, and

3. the aggregate amount of property purchased must not exceed the value of the property destroyed on the date the calamity occurred.

(d) Records. Records must be maintained to substantiate any claim of exemption pursuant to this regulation. Such records must include, but are not limited to, documents indicating the name of the purchaser, the date of purchase, the purchase price, the date the property was first brought into this state (if applicable), and the dates and locations the work of art was on display at a museum.

History—Adopted November 16, 1988, effective January 28, 1989. Adopted Regulation 1586 to exempt from tax certain purchases of public art by this state or any local governmental entity for display to the public in public places as specified.

Amended December 12, 2006, effective July 26, 2007. Amended subdivision (b)(1)(B) to incorporate new statutory language clarifying the definition of "crafts." Amended subdivision (c)(1) to incorporate a statutory change regarding leases of original works of art for 35 years or more.

Regulation 1587. Animal Life, Feed, Drugs and Medicines.

Reference: Sections 6018.1, 6358, and 6358.4, Revenue and Taxation Code.

(a) Animal Life. Tax does not apply to sales of any form of animal life of a kind the products of which ordinarily constitute food for human consumption (food animals), as for example, cattle, sheep, swine, baby chicks, hatching eggs, fish, and bees. Operative January 1, 1993, food animals include ostriches. Operative January 1, 1996, food animals include emus. Operative January 1, 2000, the term "food animals" includes any form of animal life classified by the California Department of Food and Agriculture, by regulation, as livestock or poultry intended for human consumption under sections 18848 and 25408 of the California Food and Agricultural Code. Tax shall not apply to sales of such newly defined food animals on or after the date the related California Food and Agricultural regulation is effective.

The term "food animals" does not include any forms of animal life which are commonly kept as pets or companions, the sale of which for food is prohibited by Penal Code section 598b, nor does it include any horse, the sale of which for human consumption is prohibited by Penal Code section 598c. For example, cats, dogs, horses, mink, and canaries are not food animals.

(b) Feed.

(1) Definition. The term "feed" as used herein includes codliver oil, salt, bone meal, calcium carbonate, double purpose limestone granulars and oyster shells, but does not include sand, charcoal, granite grit, sulphur and medicines. It also includes any item which is purchased for use as an ingredient of a product which would constitute a feed were the product itself sold.

(2) Application of Tax.

(A) In General. Tax does not apply to sales of feed for food animals or for any non-food animals which are to be sold in the regular course of business.

(B) Cellulose Casings. Tax does not apply to the sale or use of cellulose casings used in the manufacture and production of processed meat products which are ultimately resold as, or incorporated into, feed for food animals or non-food animals which are to be sold in the regular course of business.

(C) Medicated Feed. Tax does not apply to the sale of medicated feed, the primary purpose of which is prevention and control of disease of food animals or of non-food animals which are to be sold in the regular course of business. Tax also does not apply to sales of the particular ingredients purchased from different sellers by a purchaser who mixes them himself for feeding to such animal life, in such proportions that the product is an exempt medicated feed rather than a drug.

(c) Drugs or Medicines.

(1) Definitions. The term "drugs or medicines, the primary purpose of which is the prevention and control of disease," as used herein, means and includes any livestock drug approved by the United States Food and Drug Administration, which are defined and registered pursuant to California Food and Agricultural Code Sections 14202, 14206, and 14281. The term also includes vitamins as well as insecticides which are labeled for livestock use and which are administered directly to the livestock. The term includes, but is not limited to, legend drugs, pills and capsules, liquid medications, injected drugs, ointments, vaccines, intravenous fluids, and medicated soaps. "Livestock" includes poultry. "Livestock drug" means any drug, combination of drugs, proprietary medicine, or combination of drugs and other ingredients which is prepared for administration to livestock. On or after January 1, 1997, the term "drugs and medicines" also includes oxygen administered to food animals, as provided in (c)(2)(A) below.

(2) Application of Tax.

(A) Oxygen. On or after January 1, 1997, tax does not apply to the sale or use of oxygen administered to food animals for the primary purpose of preventing or controlling disease, including oxygen injected into ponds or tanks that house or contain aquatic species raised, kept, or used as food for human consumption. However, tax does apply to the sale or use of oxygen administered to nonfood animals whether or not the animals are being held for sale in the regular course of business.

(B) Administered Directly. Prior to January 1, 1997, except as provided in Regulation 1506 (18 CCR 1506), subdivision (h), dealing with licensed veterinarians, tax applies to the sales or use of drugs or medicines as defined in subdivision (c)(1) which are administered directly to animal life. Operative January 1, 1997, tax does not apply to the sale or use of drugs or medicines as defined in subdivision (c)(1) which are administered directly (e.g., orally, hypodermically, or topically or externally as injections, implants, drenches, repellents, or pour-ons) to food animals. The sale or use of drugs or medicines as defined in subdivision (c)(1) administered directly to non-food animals are subject to tax regardless that such animals are being held for sale in the regular course of business.

(C) Mixed with Feed or Drinking Water. Prior to April 1, 1996, tax applies to the sale or use of drugs or medicines as defined in subdivision (c)(1) administered to animal life as an additive to feed (except as provided in (b)(2)(B) above) or to drinking water. Operative April 1, 1996, tax does not apply to the sale or use of such drugs or medicines administered as an additive to, or component of, feed or drinking water for food animals or for nonfood animals being held for sale in the regular course of business.

(d) Exemption Certificates.

(1) Feed. Sellers of feed should secure feed exemption certificates with respect to sales of feed of a kind customarily used both to feed food animals and to feed non-food animals which is purchased for food animals, and with respect to sales of all feed which is purchased for non-food animals being held for sale in the regular course of business. The following form of certificate is suggested:

"I hereby certify that all of the feed which I shall purchase from __________

will be purchased for use as feed for food animals or for non-food animals which are being held for sale in the regular course of business. This certificate shall be considered a part of each order which I give unless such order shall otherwise specify. This certificate shall be good until revoked in writing.

Signature ___________

Address ___________

Occupation ___________

Seller's Permit No. (if any) ___________ "

Sellers of feed need not secure feed exemption certificates with respect to sales of feed of a kind ordinarily used only in the production of meat, dairy or poultry products for human consumption or with respect to sales in small units (two standard sacks of grain or less and/or four bales of hay or less) of feed of a kind customarily used either for food production or other purposes (feeding work stock), or with respect to sales of feed that is specifically labeled by the manufacturer for food animals. In the absence of evidence to the contrary, it will be presumed that all such feed are to be used in producing meat, dairy or poultry products for human consumption.

(2) Drugs or Medicines.

(A) Administered Directly. Operative January 1, 1997, persons who buy drugs or medicines as defined in subdivision (c)(1), which will be administered directly (e.g., orally, hypodermically, or topically or externally as injections, implants, drenches, repellents, or pour-ons) to food animals, should give the vendor an exemption certificate similar to the example in subdivision (d)(2)(C) below.

(B) To be Mixed With Feed or Drinking Water. Operative April 1, 1996, persons who buy drugs or medicines as defined in subdivision (c)(1) to be mixed with feed or drinking water, for food animals or of non-food animals being held for sale in the regular course of business, should give the vendor an exemption certificate similar to the example in subdivision (d)(2)(C) below.

(C) Sellers of drugs or medicines to be mixed with feed or drinking water for food animals or for non-food animals being held for sale in the regular course of business, to be administered directly to a food animal, or, if oxygen, administered to a food animal such as by pumping or injecting the oxygen into the animal's living environment should request a certificate similar to the following from the buyer:

"I hereby certify that the drugs or medicines which I shall purchase from ___________ will be purchased

[ ] as an additive to feed or drinking water for food animals or for non-food animals being held for sale in the regular course of business,

[ ] for administration directly to a food animal, or

[ ] for oxygen administered to a food animal.

This certificate shall be considered a part of each order which I give unless such order shall otherwise specify. This certificate shall be good until revoked in writing.

Signature ___________

Address ___________

Occupation ___________

Seller's Permit No. (if any) ___________ "

(3) Invoices Related to Exemption Certificates. Exemption certificates should be complete with the information specified in the above forms, including the names and addresses of the purchasers, in order to constitute adequate support for exemptions claimed by sellers. In addition, the invoices on sales claimed as exempt should specify the names of the purchasers in order to relate them to exemption certificates.

History—Effective July 1, 1947.

Amended July 23, 1947.

Amended and renumbered August 5, 1969, effective September 6, 1969.

Amended March 9, 1976, effective April 18, 1976. Added (c)(3) clarifying requirement of sellers to maintain completed exemption notices and related invoices.

Amended July 30, 1986, effective December 13, 1986. Amended subdivision (b)(2)(C) to provide that tax applies to sales of drugs or medicines administered to animal life directly or as an additive to drinking water except as provided.

Amended November 18, 1987, effective February 26, 1988. In subdivision (c)(1), defined term "small units" of feed.

Amended January 11, 1996, effective October 12, 1996. Amended subdivision (a) to define ostriches as food animals; added a reference to the California Code of Regulations to subdivision (b)(2)(C); corrected a clerical error in subdivision (c)(2).

Amended August 1, 1997, effective January 8, 1998. Amended subdivision (a) by adding reference to emus as food animals effective January 1, 1996. Former subdivision (b)(2)(C) redesignated (c) and renamed "Drugs or Medicines." New subdivisions (c)(1) and (c)(3) added. New subdivision (c)(2) added incorporating language of former subdivision (b)(2)(C), adding reference to use of products, cross-reference to new subdivision (c)(1), and adding new second sentence. Former subdivision (c) redesignated (d) and subdivision (d)(1) amended by adding phrase "which … business" to first paragraph; deleting language "I am engaged … that" and "in the production … products" from, and adding phrase "as feed … business" to first paragraph of certificate. New subdivision (d)(2)(A) added. First paragraph of former subdivision (c) incorporated into new subdivision (d)(2)(B) adding operative date, cross-reference to new subdivision (c)(1), phrase "or drinking … business," and cross-reference to new subdivision (d)(2)(C); second sentence deleted. Content of second paragraph of former subdivision (c)(2) incorporated into new subdivision (d)(2)(C) with phrases "or medicines", "or drinking water", and "or for non-food animals … food animal" added. In sample certificate, phrases "I … of" deleted, "or medicines" added, and language beginning with "for" and running to end of first paragraph, along with blanks, deleted; and two new blocks added.

Amended July 29, 1999, effective October 1, 1999. New subdivision (b)(2)(B) "Cellulose Casings," added. Renumbered old subdivision (b)(2)(B) "Medicated Feed," as subdivision (b)(2)(C).

Amended February 23, 2000, effective May 18, 2000. Amended subdivision (a) to include in "food animals" any form of animal life or poultry classified by the California Department of Food and Agriculture as intended for human consumption, and to clarify "food animals" do not include animal life kept as pets and companions. Amended subdivisions (c)(1) and (d)(2)(C), and added subdivision (c)(2)(A) concerning oxygen administered to food animals. Redesignated former subdivisions (c)(2)–(3) to (c)(2)(B)–(C).

Regulation 1588. Seeds, Plants and Fertilizer.

Reference: Section 6358, Revenue and Taxation Code.

(a) Seeds and Plants. Tax does not apply to sales of seeds, annual plants, and operative January 1, 1999, non-annual plants, the products of which ordinarily constitute food for human consumption or the products of which are to be sold in the regular course of the purchaser's business, including fruit trees, berry vines, and grape rootlings or rootstock, or cuttings of every variety. Tax does not apply to sales of seed, the products of which will be used as feed for any form of animal life of a kind the products of which ordinarily constitute food for human consumption or the products of which are to be sold in the regular course of the purchaser's business.

(b) Fertilizer.

(1) Definition. The term "fertilizer" includes commercial fertilizers, agricultural minerals, manure, and carbon dioxide. The terms "commercial fertilizers" and "agricultural minerals" as used herein are defined in sections 14522 (commercial fertilizer) and 14512 (agricultural minerals) of the Food and Agricultural Code. "Manure" means the excreta of any domestic animal or domestic fowl which is not artificially mixed with any material except a material which has been used for bedding, sanitary, or feeding purposes for such an animal or fowl or for the preservation of the manure. The term "fertilizer" does not include "packaged soil amendments" or "auxiliary soil and plant substances" as these terms are defined (with the exception noted below) in sections 14552 (packaged soil amendments) and 14513 (auxiliary soil and plant substances) of the Food and Agricultural Code. For the purposes of this regulation, "manures sold without guarantees for plant nutrients" as described in section 14552 of the Food and Agricultural Code are not packaged soil amendments and carbon dioxide is not an auxiliary soil and plant substance as that term is defined in section 14513 of the Food and Agricultural Code.

(2) Application of Tax. Tax does not apply to sales of fertilizer to be applied to land or in foliar application the products of which are to be: (a) used as food for human consumption, (b) used as feed for any form of animal life of a kind the products of which ordinarily constitute food for human consumption, or (c) sold in the regular course of the purchaser's business.

When insecticides are mixed with fertilizer and the mixture sold, that portion of the total price allocable to the fertilizer may be excluded from the measure of the tax if the mixed product is applied to land or in foliar application the products of which are to be: (a) used as food for human consumption, (b) used as feed for any form of animal life of a kind the products of which ordinarily constitute food for human consumption, or (c) sold in the regular course of the purchaser's business.

History—Adopted as of January 1, 1945, as a restatement of previous rulings.

Amended and renumbered March 24, 1970, effective April 29, 1970.

Amended August 20, 1985, effective November 22, 1985. In Subdivision (b)(1), defined the term "fertilizer" to include the terms "commercial fertilizers," "agricultural minerals," and "manures" as those terms are defined in the Food and Agricultural Code and provided this term does not include soil amendments nor does it include auxiliary soil and plant substances. Corrected references to sections of the Food and Agricultural Code and defined the term "manure". Deleted the footnote which repeated the text of the applicable Food and Agricultural Code sections.

Amended August 24, 1988, effective November 18, 1988. In subdivision (a) amended to provide that effective October 1, 1987, nonannual plants, such as fruit trees and berry vines, which are eligible to be purchased with federal food stamp coupons and are so purchased are exempt from the sales and use taxes.

Amended July 30, 1992, effective January 10, 1993. Paragraph (a) was amended to make clear that tax does not apply to sales of seed which will be used to grow feed for any animals which ordinarily constitute food for human consumption and not just for livestock and poultry. Paragraph (b)(1) was amended to correct references to sections of the Food and Agricultural Code. Paragraph (b)(2) was amended to clarify that to be exempt, the products grown must be used as food for human consumption or sold in the regular course of business and that the exemption applies to fertilizer which has been mixed with insecticides when sold for the same purposes as unmixed fertilizer.

Amended January 22, 1999, effective April 1, 1999. In subdivision (a), new second sentence added; un-numbered paragraph deleted. Phrase "are to be" replaced with "(c)" in subdivision (b)(2).

Amended October 7, 1999, effective December 3, 1999. Deleted reference to section 6373 of the Revenue and Taxation Code concerning food stamps as obsolete. Prior to January 1, 1999 sales of non-annual plants were taxable unless purchased with food stamp coupons. After operative date of amendment to section 6358 (Statutes of 1998, Chapter 323, (AB-2798)) sales of non-annual plants the products of which are food for human consumption became not taxable regardless of method of payment. Subdivision (a) corrected operative date to January 1, 1999 to comply with statutory change to section 6358 by AB 2798. Also added the words "or rootstock" after the word "rootlings" to recognize that they are synonymous terms used by the grape and tree fruit industry.

Amended October 19, 2004, effective January 13, 2005. Subdivision (a)-first sentence- comma added after "seeds" and word "and" before "annual plants" deleted and phrase ", and operative January 1, 1999, non annual plants," added after word "plants" and phrase "the products of which" added after word "or" and period deleted; second sentence- phrase "Operative … consumption," deleted to combine remainder of second sentence with first; third sentence- phrase "the products of which" added after word "or."

Amended December 18, 2014, effective April 1, 2015. Subdivision (b)(1) deleted "and" from before "manure" in and added "and carbon dioxide" at the end of the first sentence, added the word "packaged" before each reference to soil amendments, added "the" after "for" in and added "and carbon dioxide is not an auxiliary soil and plant substance as that term is defined in section 14513 of the Food and Agricultural Code" to the end of the last sentence, and changed each reference to "Sections" or "Section" to "sections" or "sections." Subdivision (b)(2) and the last unnumbered paragraph in subdivision (b) added "or in" before "foliar application," and deleted the parenthesis around and "including" from before "foliar application."

Regulation 1589. Containers and Labels.

Reference: Sections 6007, 6008, 6009, 6012, 6364, and 6364.5, Revenue and Taxation Code.

(a) Definitions. The term "containers" as used herein means the articles in or on which tangible personal property is placed for shipment and delivery such as wrapping materials, bags, cans, twines, gummed tapes, barrels, boxes, bottles, drums, carboys, cartons, sacks, pallets and materials from which such containers are manufactured.

The term "returnable containers" as used herein means containers of a kind customarily returned or resold by the buyers of the contents for re-use by the packers, bottlers or sellers of the commodities contained therein. A container, title to which is retained by the seller or for which a deposit is taken by such seller, is a returnable container.

A container used for shipment or delivery of food for human consumption is not customarily returned by the buyer when:

1. The container is sold together with the contents;

2. No deposit is charged on the container;

3. Title to the container is not retained;

4. There is no obligation to repurchase the container;

5. The container is of the type that is fungible; and

6. The container is repurchased without regard to whether it is the same container originally sold.

Example: A tomato paste processor purchased a new or used container. The processor fills the container with tomato paste or other processed food. The tomato paste, together with the container, is sold to a spaghetti sauce manufacturer. No deposit is charged on the container, title to the container is not retained, and there is no obligation to repurchase the container. The container is of a type that is fungible. The spaghetti sauce manufacturer sells the container to a warehouse or a food processor who in turn sells containers that may or may not include the original container to a tomato paste processor that may or may not be the original purchaser. This container is not customarily returned by the buyer.

Examples of returnable containers are: registered dairy products containers, steel drums, certain types of beer and soft drink bottles, wine barrels, chemical carboys, and gas cylinders.

All other containers are "nonreturnable containers." Examples of nonreturnable containers are: wrapping and packing materials, paper bags, twine, cartons, cans, medicine and distilled spirits bottles.

The term "deposit" as used herein means an amount charged to the purchaser of the contents of the container with the understanding that such amount will be repaid when the container or a similar container is delivered to the seller. The term "deposit" as used herein does not include amounts representing redemption or recycling values of beverage containers pursuant to division 12.1 (commencing with Section 14500) of the Public Resources Code whether or not such amounts are separately stated to the purchaser of the contents of the container.

(b) Application of Tax.

(1) Containers. Tax does not apply to the sale of, and the storage, use or other consumption of:

(A) Nonreturnable containers when sold or leased without the contents to persons who place the contents in the container and sell the contents together with the container.

(B) Nonreturnable containers when sold without the contents to persons who place food products for human consumption in the containers for subsequent sale.

(C) Returnable containers when sold with the contents in connection with a retail sale of the contents, or when resold for refilling. In the case of a lease of a returnable container that is a continuing sale, the lessor's first lease of the container for filling is taxable for the full term of the lease or thirty (30) days whichever is greater. The lessor's subsequent lease of the container for refilling for sale with the contents is not taxable.

(D) All containers when sold or leased with the contents, if the sales price of the contents is not required to be included in the measure of the sales tax or the use tax.

(E) Operative April 1, 2000, all containers when sold or leased without the contents to persons who place food products for human consumption in the containers for shipment, provided the food products will be sold. The exemption applies without regard to whether the food products are sold in the same container or not, or whether the food products are remanufactured or repackaged prior to their sale.

Tax applies to all other sales of containers except sales for the purpose of resale to other sellers of containers who purchase them for resale without the contents.

Operative April 1, 1998, tax does not apply to the sale or to the storage, use, or other consumption of any container used to collect or store human whole blood, plasma, blood products, or blood derivatives held for medical purposes, including, but not limited to, blood collection units and blood pack units.

Deposits as defined herein are not taxable.

(2) Labels. Tax does not apply to sales of labels or name-plates if:

(A) The purchaser affixes them to property to be sold and sells them along with and as a part of such property, as, for example, sales of name-plates of manufacturers or producers which are permanently affixed to each unit of products sold, such as automobiles and machinery.

(B) The purchaser affixes them to nonreturnable containers of property to be sold, or to returnable containers of such property if a new label is affixed to the container each time it is refilled. Examples are sales of labels to be affixed to fruit boxes, cans, bottles and packing cases, to growers, packers, bottlers and others who place the contents in the containers.

(c) Particular Applications.

(1) Price Tags. Tax applies to sales of such items as price tags, shipping tags and advertising matter used in connection with the sale of property or enclosed with the property sold.

(2) Feed Analysis Tags. Tax does not apply to sales of feed analysis tags to be attached to containers of feeds and sold along with the container and contents.

(3) Feed Bags. Feed bags sold to feed dealers who place feed in the bags and sell the feed together with the bags are nonreturnable containers,* and the sale of such bags to feed dealers is not taxable. It is immaterial whether the bags are made of burlap, cotton, paper, or other material, or whether there is a brand name or dealer's name imprinted on the bags.

If, however, any feed dealer charges a deposit to customers to secure the return of the bags, or otherwise requires his customers to return the bags to him, the bags become returnable containers and tax applies to the sale of the bags to the feed dealer.

(4) Gift Wrapping. Tax applies to the entire charge for "gift wrapping" (i.e., furnishing the materials and labor required to wrap an item for a customer so as to be suitable for use by him as a gift), whether or not the person who does the gift wrapping is the seller of the contents. If the person who does the gift wrapping is the seller of the contents, the gift wrapping is considered sold together with the contents, whether or not a separate charge is made for the gift wrapping. The person who does the gift wrapping may purchase the materials free of tax for resale.

However, tax does not apply to charges for gift wrapping exempt food products sold by the person who does the gift wrapping, unless the value of the gift wrapping exceeds the value of the food products.

* The conclusion that feed bags are nonreturnable containers resulted from a statewide survey made by the board with the cooperation of the California Grain and Feed Association, which showed that substantially less than 50 percent of the feed bags are returned to the feed dealers by their customers for re-use.

History—Effective August 1, 1933.

Adopted January 1, 1945, as a restatement of previous rulings.

Amended and renumbered August 5, 1969, effective September 6, 1969.

Amended May 21, 1975, effective June 29, 1975. Deleted cement bags as returnable containers and added (c)(4) classifying gift wrappers as resellers and their labor as fabrication.

Amended October 7, 1987, effective December 30, 1987. In subdivision (a), expanded the definition of the term "deposit" to exclude redemption or recycling values of beverage containers in order to prevent any confusion which may arise when the California Beverage Container Recycling and Litter Reduction Act becomes effective. Because redemption or recycling values of beverage containers are not considered deposits, they therefore are includable in the gross receipts of the seller of the containers.

Amended April 23, 1996, effective August 8, 1996. New subdivision (b)(1)(B) added; existing subdivisions (b)(1)(B) and (C) re-designated (b)(1)(C) and (D), respectively. Obsolete effective date deleted from subdivision (c)(4).

Amended June 11, 1998, effective July 11, 1998. Amended subdivision (b) to incorporate provisions of Chapter 773, Statutes of 1997.

Amended July 29, 1999, effective October 15, 1999. Subdivision (a): phrase "of the contents" deleted from second sentence in the first unnumbered paragraph; also new unnumbered second and third paragraphs added. Subdivision (b)(1)(C): new second and third sentence added. Subdivision (b)(1)(D) the words "or leased" added to the first paragraph after the word "sold".

Amended October 19, 2004, effective January 13, 2005. Subdivision (b)(1)—word "the" added before word "sales" and phrase ", and the storage, use, or other consumption of:" added to end of subdivision to clarify that the exemptions listed therein apply to both sales and use tax. Subdivision (b)(1)(E) added.

Regulation 1590. Newspapers and Periodicals.

Reference: Sections 6005, 6006, 6007, 6010, 6015, 6361.5, 6362.7, and 6362.8, Revenue and Taxation Code.

(a) Definitions.

(1) "Digital-Only Subscription." A "digital-only subscription" means a subscription to access digital content from a newspaper publisher, without any print edition delivery.

(2) "Digital-Only Subscription Rate." "Digital-only subscription rate" means the average of all the actual rates a newspaper publisher charges its customers for digital-only subscriptions, except the rates for promotional or introductory subscriptions as defined in subdivision (a)(12).

(3) "Distributor." "Distributor" means any person who acquires newspapers or periodicals for subsequent distribution to retailers or newspaper carriers.

(4) "Ingredient or Component Part of a Newspaper or Periodical." The term "ingredient or component part of a newspaper or periodical" includes only those items that become physically incorporated into the publication and not those which are merely consumed or used in the production of the publication. For example, newsprint and ink are ingredients of a newspaper; however, a photograph does not become an ingredient or component part of a newspaper or periodical merely because the image of the photograph is reproduced in the publication.

Handbills, circulars, flyers, order forms, reply envelopes, maps or the like are component parts of a newspaper or periodical when attached to or inserted in and distributed with the newspaper or periodical.

(5) "Mixed Newspaper Subscription." "Mixed newspaper subscription" means and includes a subscription for delivery of the print edition of a newspaper to a location provided by the customer and access to digital content from the newspaper publisher.

(6) "Mixed Newspaper Subscription Rate." "Mixed newspaper subscription rate" means the total amount a newspaper publisher charges its customer for a mixed newspaper subscription, including any charges for transportation and sales tax reimbursement.

(7) "Newspaper." The term "newspaper" as used herein is limited to those publications which are commonly understood to be newspapers and which are printed and distributed periodically at daily, weekly, or other short intervals for the dissemination of news of a general character and of a general interest. The term does not include handbills, circulars, flyers, or the like, unless distributed as a part of a publication which constitutes a newspaper within the meaning of this subdivision. Neither does the term include any publication which is issued to supply information on certain subjects of interest to particular groups, unless such publication otherwise qualifies as a newspaper within the meaning of this subdivision. For purposes of this subdivision, advertising is not considered to be news of a general character and of a general interest.

(8) "Newspaper Carrier." "Newspaper carrier" means any person who acquires newspapers from a publisher or distributor to deliver to consumers. The term includes a hawker. A "hawker" is an individual who sells single copies of newspapers to passersby on a street corner or other trafficked area. "Newspaper carrier" does not include persons selling newspapers or periodicals from a fixed place of business.

(9) "Periodical." The term "periodical" as used herein is limited to those publications which appear at stated intervals, each issue of which contains news or information of general interest to the public, or to some particular organization or group of persons. Each issue must bear a relationship to prior or subsequent issues in respect to continuity of literary character or similarity of subject matter, and there must be some connection between the different issues of the series in the nature of the articles appearing in them.* Each issue must be sufficiently similar in style and format to make it evident that it is one of a series. An annual report of a corporation which is substantially different in style and format from the corporation's quarterly reports is not part of a series with the quarterly reports. The term "periodical" does not include books complete in themselves, even those that are issued at stated intervals, for example, books sold by the Book-of-the-Month Club or similar organizations; so-called "pocket books," a new one of which may be issued once a month or some other interval; or so-called "one-shot" magazines that have no literary or subject matter connection or continuity between prior or subsequent issues. The term does not include catalogs, programs, score-cards, handbills, price lists, order forms or maps. Neither does it include shopping guides or other publications of which the advertising portion, including product publicity, exceeds 90 percent of the printed area of the entire issue in more than one-half of the issues during any 12-month period.

(10) "Print-Only Subscription." A "print-only subscription" means a subscription for delivery of the print edition of a newspaper delivered to a location provided by the customer, without any access to digital content.

(11) "Print-Only Subscription Rate." "Print-only subscription rate" means the average of all the actual rates a newspaper publisher charges its customers for print-only subscriptions, inclusive of any charges for transportation and sales tax reimbursement, except the rates for promotional or introductory subscriptions as defined in subdivision (a)(12).

(12) "Promotional or Introductory Subscriptions." "Promotional or introductory subscriptions" means subscriptions that are sold for a substantially discounted rate, usually to new subscribers, and that are generally limited to a specified period of time after which the prices of the subscriptions increase. Promotional or introductory subscriptions include, but are not limited to, subscriptions sold for substantially discounted rates referred to as sales rates, limited-time rates, or seasonal rates.

Example 1: Newspaper publisher ABC offers a new customer a four-week unlimited digital-only subscription for a $1.00 introductory rate. After the four-week introductory period, the customer is then charged $16.00 every four weeks. In this instance, the introductory rate the customer paid is substantially less than the post-introductory rate. Therefore, the introductory subscription rate is not included in the calculation of ABC’s digital-only subscription rate.

Example 2: Newspaper publisher XYZ’s full print-only subscription rate is $169 for 26 weeks ($6.50 per week). XYZ offers new customers and existing monthly subscribers a promotional rate for its print-only subscription of $3.25 per week for a term of 26 weeks (a savings of 50% off the full print-only subscription rate). In this instance, the promotional rate is substantially less than the full print-only subscription rate. Therefore, the promotional subscription rate is not included in the calculation of XYZ’s print-only subscription rate.

Example 3: Newspaper publisher ABC’s customer Mr. Y has had a print-only subscription for the past three years for which he currently pays the full subscription rate of $5.00 per week. When Mr. Y requests to cancel his subscription, ABC offers to reduce his subscription rate to $4.25 per week (a savings of 15% off the full subscription rate he was paying), for an indefinite period. In this instance, the discounted subscription rate offered to retain Mr. Y is not substantially less than the full subscription rate. Therefore, the discounted subscription rate is included in the calculation of ABC’s print-only subscription rate.

(13) "Publisher." "Publisher" means and includes any person who owns the rights to produce, market, and distribute printed literature and information.

(14) "Tangible Personal Property Allocation Percentage." The "tangible personal property allocation percentage" means the percentage of a mixed newspaper subscription rate that is for the sale of tangible personal property, inclusive of any charges for transportation and sales tax reimbursement.

(15) "Third-Party Retailer." "Third-party retailer" means and includes any person who makes retail sales of subscriptions to newspapers and periodicals who is not the publisher of the newspapers or periodicals. Typically, third-party retailers solicit subscriptions in a single offering for a large number of different publications, require that payment be made to the account of the third-party retailer, and undertake to resolve subscription problems. "Third-party retailer" does not include persons who solicit renewals of subscriptions on behalf of individual publishers.

(b) Application of Tax.

(1) In General. The sale of newspapers and periodicals, including sales by third party retailers, is subject to tax unless otherwise exempt.

Tax does not apply to sales of tangible personal property to persons who purchase the property for incorporation as a component part of a newspaper or periodical which will be sold notwithstanding that the purchaser is not the seller of the newspaper or periodical.

See Regulation 1574 for the application of tax to sales through vending machines and Regulation 1628 for the application of tax to transportation charges.

(2) Distributions of Newspapers and Periodicals Without Charge. Tax does not apply to the sale or use of tangible personal property which becomes an ingredient or component part of a copy of a newspaper or periodical regularly issued at average intervals not exceeding three months when that copy of such newspaper or periodical is distributed without charge, nor does tax apply to such distribution.

Newspapers and periodicals distributed on a voluntary pay basis shall be considered as distributed without charge. Newspapers and periodicals are distributed on a voluntary pay basis when payment is requested from the consumer but is not required.

(3) Subscriptions.

(A) Exempt Subscriptions. Tax does not apply to the sale or use of a periodical, including a newspaper, which appears at least four, but not more than 60 times each year, which is sold by subscription, and which is delivered by mail or common carrier. For example, a daily newspaper is not a periodical for the purposes of this subdivision. Tax does not apply to the sale or use of tangible personal property which becomes an ingredient or component part of such a periodical.

(B) Mixed Newspaper Subscriptions. When a newspaper publisher sells a mixed newspaper subscription, tax applies to the sale of the print edition of the newspaper delivered to the location provided by the customer (unless otherwise exempt or excluded), and not the access to digital content. To determine the percentage of a mixed newspaper subscription rate that is for the print edition of a newspaper delivered to a location provided by the customer, inclusive of any charges for transportation and sales tax reimbursement, a newspaper publisher must multiply the rate charged to the customer by the newspaper publisher’s tangible personal property allocation percentage.

1. For sales of mixed newspaper subscriptions made on and after October 1, 2016, a newspaper publisher’s tangible personal property allocation percentage is presumed to be forty-seven (47) percent. Fifty-three (53) percent of the mixed newspaper subscription rate is presumed to be for the nontaxable sale of access to digital content.

2. A newspaper publisher may rebut the presumptions and establish a lower tangible personal property allocation percentage by demonstrating to the satisfaction of the Department that its print-only subscription rate divided by the sum of its print-only subscription rate and digital-only subscription rate is less than forty-seven (47) percent. A newspaper publisher shall maintain records pursuant to Regulation 1698, Records, to substantiate that the presumption is rebutted. Percentages shall not be computed more often than once per quarter.

3. The following formula may be used to determine the measure of tax when a mixed newspaper subscription rate includes nontaxable transportation charges and sales tax reimbursement:

MSR = Mixed Newspaper Subscription Rate

NTC = Nontaxable Transportation Charges

AP = Tangible Personal Property Allocation Percentage (Decimal form)

TR = Applicable Tax Rate (Decimal form)

Measure of Tax = [((MSR×AP)-NTC)/(1+TR)]

The following example illustrates the calculation of the measure of tax for a mixed newspaper subscription when the mixed newspaper subscription rate (including sales tax reimbursement and nontaxable transportation charges) is $100, the newspaper publisher’s tangible personal property allocation percentage is 47 percent (.47), the nontaxable transportation charges are $10, and the applicable tax rate is 8 percent (.08).

| Measure of Tax = [(($100×.47)-$10)/(1+.08)] | Total |

|---|---|

| Amount for the Sale of the Print Edition of the Newspaper Delivered

(Including Sales Tax Reimbursement and Nontaxable Transportation Charges) |

$47.00 |

| Amount for the Sale of the Print Edition of the Newspaper Delivered Excluding Nontaxable Transportation Charges

(Including Sales Tax Reimbursement) |

$37.00 |

| Measure of Tax for the Sale of the Mixed Newspaper Subscription

($37.00 / 1.08) |

$34.26 |

| Sales Tax Due

($34.26 x .08) |

$2.74 |

| Amount for the Nontaxable Sale of Access to Digital Content

($100.00 x .53) |

$53.00 |

(C) Reporting Subscription Sales. Each delivery of a newspaper or periodical pursuant to a subscription sale is a separate sale transaction. When the sale is subject to tax, the retailer must report and pay the tax based upon the reporting period within which the delivery is made. The subscription price shall be prorated over the term of the subscription period.

(4) Membership Organizations. Generally, tax applies to sales of newspapers and periodicals by membership organizations. If the price is separately stated, tax applies to that amount. If the price is not separately stated, the measure of tax is the fair retail selling price of the publication.

The application of tax to distributions of newspapers and periodicals by nonprofit organizations is provided in subdivision (b)(5). The application of tax to sales of periodicals by subscription is provided in subdivision (b)(3).

(5) Nonprofit Organizations.

(A) Internal Revenue Code Section 501(c)(3) Organizations. Tax does not apply to the sale or use of any newspaper or periodical distributed by an organization that qualifies for tax exempt status under section 501(c)(3) of the Internal Revenue Code, nor tangible personal property which becomes an ingredient or component part of any such newspaper or periodical regularly issued at average intervals not exceeding three months and distributed under either of the following circumstances:

1. The issues are distributed to the organization's members in consideration of the organization's membership fee; or

2. The issues are of a newspaper or periodical which neither receives revenue from, nor accepts, any commercial advertising.

For purposes of this subdivision, any governmental entity established and administered for the purposes provided in Internal Revenue Code section 501(c)(3) shall be considered to be an organization that qualifies for tax exempt status under that section.

(B) Other Nonprofit Organizations. Tax does not apply to the sale or use of any newspaper or periodical regularly issued at average intervals not exceeding three months and distributed by a nonprofit organization, nor tangible personal property that becomes an ingredient or component part of any such newspaper or periodical, only as to issues distributed pursuant to both of the following requirements:

1. The issues are distributed to the organization's members in consideration, in whole, or in part, of the organization's membership fee;

2. The amount paid or incurred by the nonprofit organization for the cost of printing the newspaper or periodical is less than ten percent of the membership fee attributable to the period for which the newspaper or periodical is distributed, whether the publication is printed within or without this state. The cost of printing shall be determined as follows.

The cost of printing includes costs of tangible personal property purchased to become an ingredient or component part of the newspaper or periodical (e.g., ink and paper) and costs of labor to print the newspaper or periodical. The cost of printing does not include costs not attributable to actual printing, such as costs of special printing aids, typography, and preparation of layouts.

If the organization contracts with an outside printer to print the newspaper or periodical, the organization shall obtain and retain documentation segregating the costs of printing from the printer's other charges.

If the organization is the printer of the newspaper or periodical, the cost of printing includes the aggregate of the cost of tangible personal property purchased to become an ingredient or component part of the newspaper or periodical; labor of printing, including fringe benefits and payroll taxes; and other costs attributable to the actual printing of the newspaper or periodical.

If an organization has published the newspaper or periodical for a period exceeding twelve months and the method of printing has not changed, the organization may elect to consider the cost of printing for a reporting period to be equal to the amount paid or incurred for the same reporting period for the previous fiscal or calendar year.

(6) Newspaper Carriers. A newspaper carrier is not a retailer. The publisher or distributor for whom the carrier delivers is the retailer of the newspapers delivered. The publisher or distributor shall report and pay tax measured by the price charged to the customer by the carrier.

(7) Consumption of Property. Tax applies to the sale to or use by a newspaper or periodical publisher of tangible personal property consumed in the manufacturing process. Tax does not apply to the cost of tangible personal property lost or wasted in the manufacturing process when that property was purchased for the purpose of incorporation into a newspaper or periodical to be sold or to be distributed in accordance with subdivision (b)(2).

(8) School Catalogs and Yearbooks. Public or private schools, county offices of education, school districts, or student organizations are the consumers of catalogs and yearbooks prepared for or by them, and tax does not apply to their receipts from the distribution of the publications to students.

Tax applies to charges for the preparation of such publications made to public or private schools, county offices of education, school districts, or student organizations by printers, engravers, photographers and the like.

(c) Exemption Certificates. Any seller claiming a transaction as exempt from sales tax pursuant to Revenue and Taxation Code sections 6362.7 or 6362.8 should timely obtain in goo faith an exemption certificate in writing from the purchaser. The exemption certificate will be considered timely if obtained by the seller at any time before the seller bills the purchaser for the property, or any time within the seller's normal billing and payment cycle, or any time at or prior to delivery of the property.

(1) Certificate A. Certificate to be used for purchases of tangible personal property for incorporation into newspapers or periodicals for sale in accordance with subdivisions (b)(1) or (b)(3), above.

(2) Certificate B. Certificate to be used for purchases of tangible personal property that becomes an ingredient or component part of newspapers or periodicals that are distributed without charge in accordance with subdivision (b)(2), above.

(3) Certificate C. Certificate to be used for purchases of tangible personal property that becomes an ingredient or component part of newspapers or periodicals that are distributed by organizations which qualify for tax-exempt status under Internal Revenue Code section 501(c)(3) in accordance with subdivision (b)(5)(A), above.

(4) Certificate D. Certificate to be used for purchases of tangible personal property that becomes an ingredient or component part of newspapers or periodicals that are distributed by nonprofit organizations in accordance with subdivision (b)(5)(B), above.

* This definition is based upon Houghton v. Payne (1904) 194 U.S. 88 [48 L.Ed 888] and Business Statistics Organization, Inc. v. Joseph (1949) 299 N.Y. 443 [87 N.E.2d 505].

Certificate A

California Sales Tax Exemption Certificate

Sales of tangible personal property for

incorporation into a newspaper or periodical for sale

(Name of Purchaser)

(Address of Purchaser)

I HEREBY CERTIFY:

Initial one of the following:

________ That I hold valid seller's permit No. ________ issued pursuant to the Sales and Use Tax Law.

________ That I do not hold a seller's permit issued pursuant to the Sales and Use Tax Law. I do not sell any tangible personal property for which a permit is required.

I further certify that the tangible personal property described herein which I shall purchase from

(Name of Vendor)

will become a component part of the newspaper or periodical

(Name and Type of Newspaper or Periodical)

and sold as a component part of the publication.

I understand that in the event any such property is sold or used other than as specified above or used other than for retention, demonstration, or display while holding it for sale in the regular course of business, I am required by the Sales and Use Tax Law to report and pay any applicable sales or use tax. Description of the property to be purchased:

Date:________

(Signature of Purchaser or Authorized Agent)

(Title)

Certificate B

California Sales Tax Exemption Certificate

Sales of tangible personal property which becomes an ingredient or component part of newspapers or periodicals that are distributed without charge

(Name of Purchaser)

(Address of Purchaser)

I HEREBY CERTIFY:

Initial one of the following:

________ That I hold valid seller's permit No. ________ issued pursuant to the Sales and Use Tax Law.

________ That I do not hold a seller's permit issued pursuant to the Sales and Use Tax Law. I do not sell any tangible personal property for which a permit is required.

I further certify that I am engaged in the business of publishing

(Name and Type of Newspaper or Periodical)

which is regularly issued at average intervals not exceeding three months and distributed without charge by me. The tangible personal property described herein which I shall purchase from

(Name of Vendor)

will become a component part of the publication listed above. I understand that if I use any of the property purchased for any other purpose I am required by the Sales and Use Tax Law to report and pay any applicable sales and use tax, measured by the purchase price of such property.

Description of property to be purchased:

Date:________

(Signature of Purchaser or Authorized Agent)

(Title)

Certificate C

California Sales Tax Exemption Certificate

Sales of tangible personal property that becomes an ingredient or component of newspapers or periodicals that are distributed by organizations which qualify for tax-exempt status under Internal Revenue Code section 501(c)(3)

(Name of Purchaser)

(Address of Purchaser)

I HEREBY CERTIFY:

Initial one of the following:

________ That the purchaser holds valid seller's permit No. ________ issued pursuant to the Sales and Use Tax Law.

________ That the purchaser does not hold a seller's permit issued pursuant to the Sales and Use Tax Law. The purchaser does not sell any tangible personal property for which a permit is required.

I further certify that the purchaser is an organization that qualifies for tax-exempt status under section 501(c)(3) of the Internal Revenue Code and is engaged in the business of selling or publishing

(Name and Type of Newspaper or Periodical)

which is regularly issued at average intervals not exceeding three months.

The tangible personal property described herein which I shall purchase from

(Name of Vendor)

will be resold in the form of tangible personal property or will become a component part of a newspaper or periodical distributed by the organization and (check one or both):

________ The organization will distribute the newspaper or periodical to the members of the organization in consideration of payment of the organization's membership fee or to the organization's contributors,

________ The publication does not receive revenue from or accept any commercial advertising.